SIE vs Series 6

The SIE is the entry-level prerequisite exam that anyone 18+ can take without firm sponsorship — it proves foundational securities knowledge. The Series 6 is a limited license exam that requires both the SIE and firm sponsorship, authorizing you to sell only mutual funds, variable annuities, variable life insurance, and 529 plans. You must pass the SIE before taking the Series 6. The Series 6 is the most popular license at banks and insurance companies, but it cannot be used to sell individual stocks, bonds, options, or ETFs — those require the broader Series 7.

Side-by-Side Comparison

| Feature | SIE | Series 6 |

|---|---|---|

| Full Name | Securities Industry Essentials Exam | Investment Company and Variable Contracts Products Representative Exam |

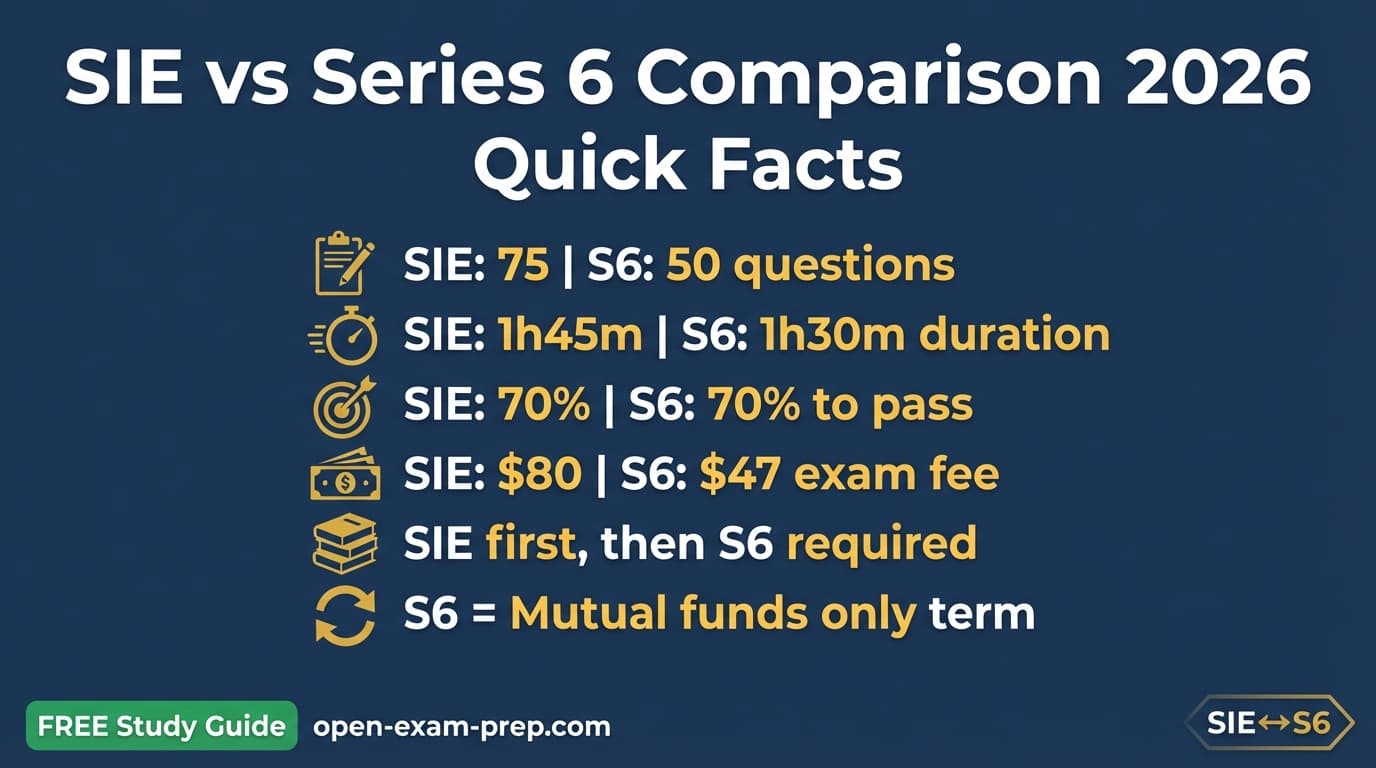

| Exam Cost | $80 | $47 |

| Passing Score | 70% (56 of 80 scored questions) | 70% (35 of 50 scored questions) |

| Questions | 85 (75 scored + 10 unscored) | 55 (50 scored + 5 unscored) |

| Time Limit | 1 hour 45 minutes | 1 hour 30 minutes |

| Study Time | 40 - 60 hours over 2 - 4 weeks | 30 - 50 hours over 2 - 4 weeks |

| Difficulty | Entry-level | Moderate |

| Prerequisites | None — anyone 18+ can take it without firm sponsorship | SIE exam passed + firm sponsorship (Form U4 filing) required |

| Exam Body | FINRA | FINRA |

Key Differences

- 1The SIE is a prerequisite exam; the Series 6 is the actual license. Passing the SIE alone does not authorize you to sell any investment products.

- 2The SIE can be taken without firm sponsorship by anyone 18+; the Series 6 requires an employing broker-dealer or bank to file Form U4 on your behalf.

- 3The SIE costs more than the Series 6 ($80 vs $47), which surprises many candidates — the prerequisite is more expensive than the license exam itself.

- 4The SIE has a higher pass rate (~74%) than the Series 6 (~58%), despite the Series 6 being a "limited" license. The Series 6 tests deep product-specific knowledge that many candidates underestimate.

- 5The SIE covers the broad securities landscape (stocks, bonds, options, regulations); the Series 6 focuses narrowly on investment companies, variable contracts, retirement plans, and tax regulations.

- 6The SIE result is valid for 4 years without firm association; the Series 6 license requires ongoing continuing education and lapses after 2 years of non-association with a firm.

- 7The Series 6 is a LIMITED license — holders can only sell mutual funds, variable annuities, variable life insurance, and 529 plans. They cannot sell individual stocks, bonds, options, ETFs, or direct participation programs.

- 8Many Series 6 holders eventually upgrade to the Series 7 for broader product authority, but they must pass a separate full-length Series 7 exam — the Series 6 does not provide any credit toward the Series 7.

What Each Exam Allows You To Do

SIE

- Demonstrate foundational knowledge of the securities industry

- Satisfy the prerequisite for all FINRA representative-level exams (Series 6, 7, 57, 79, etc.)

- Show prospective employers you are serious about a career in finance

- Begin job hunting at broker-dealers, banks, and insurance companies with a credential on your resume

Series 6

- Sell mutual funds (open-end investment companies) to retail clients

- Sell variable annuities and variable life insurance policies

- Sell 529 college savings plans and education savings accounts

- Sell unit investment trusts (UITs) that hold mutual fund shares

- Work as a bank investment representative recommending packaged investment products

- Serve insurance clients who want variable products tied to securities markets

Who Should Take Each Exam?

Take the SIE if you...

- →Career changers exploring financial services

- →College students or recent graduates getting a head start

- →Job seekers who want to prove securities knowledge before landing a firm

- →Anyone preparing for the Series 6, Series 7, or another FINRA representative exam

Take the Series 6 if you...

- →Bank investment representatives and bank financial consultants

- →Insurance agents who want to sell variable annuities and variable life insurance

- →Professionals focused exclusively on mutual funds and retirement products

- →Anyone starting in financial services who plans to upgrade to Series 7 later

Which Should You Take First?

You MUST take the SIE first — it is a mandatory prerequisite for the Series 6 (and all other FINRA representative-level exams). The optimal strategy for most bank and insurance professionals is: (1) Study for and pass the SIE while job hunting — since it requires no sponsorship, you can take it on your own timeline. (2) Use your SIE credential to strengthen your resume and interviews at banks, insurance companies, and broker-dealers. (3) Once hired, your firm will sponsor you for the Series 6 via Form U4. (4) Study for and pass the Series 6 within your firm's training window (typically 90-120 days). Because the SIE covers products and risks broadly — including mutual funds, variable products, and investment company structures — the overlap with Series 6 material is significant. Passing the SIE first gives you a strong foundation in the exact product categories the Series 6 tests in greater depth. Many candidates complete both exams within 6-8 weeks total when studying sequentially. However, before committing to the Series 6 path, consider whether the Series 7 might be a better long-term choice. The Series 6 limits you to packaged products; the Series 7 opens the full securities universe. If there is any chance you will want to sell stocks, bonds, options, or ETFs in the future, starting with the Series 7 saves you from having to take a second top-off exam later.

At a Glance: SIE vs Series 6

Exam Cost

$80

SIE

$47

Series 6

Pass Rate

~74%

SIE

~58%

Series 6

Study Time

40-60 hrs

SIE

30-50 hrs

Series 6

Median Salary

N/A (prerequisite)

SIE

$61,000

Series 6

SIE

Career changers exploring finance, college students, and anyone wanting to demonstrate securities knowledge without firm sponsorship

Series 6

Bank investment representatives, insurance agents selling variable products, and professionals focused exclusively on mutual funds, variable annuities, and 529 plans

Start preparing today:

Key Facts: SIE vs Series 6

- 1The SIE exam costs $80 and can be taken by anyone 18+ without firm sponsorship, while the Series 6 costs only $47 but requires both the SIE and sponsorship by a FINRA-member firm.

- 2The Series 6 has a significantly lower pass rate (~58%) than the SIE (~74%), despite being a limited license — candidates frequently underestimate the depth of product knowledge required.

- 3Series 6 holders can only sell mutual funds, variable annuities, variable life insurance, 529 college savings plans, and certain UITs — they cannot sell individual stocks, bonds, options, or ETFs.

- 4The SIE result is valid for 4 years without firm association, giving candidates time to secure employment before taking the Series 6.

- 5Bank investment representatives with a Series 6 license earn a median salary of approximately $61,000 per year, with top performers at major banks exceeding $86,000.

- 6The Series 6 exam has only 50 scored questions in 1 hour 30 minutes, but 36% of the exam focuses on investment company products (mutual funds) and 21% covers retirement plans and education savings.

- 7Many Series 6 holders eventually upgrade to the Series 7 for broader product authority, but they must pass the full 125-question Series 7 exam — there is no abbreviated upgrade path.

- 8The total cost to become a fully licensed Series 6 representative (SIE + Series 6 + Series 63 + prep courses + background check) ranges from $350 to $725, making it one of the most affordable professional licenses in financial services.

- 9The Series 6 is the most common license at major banks like JPMorgan Chase, Bank of America, Wells Fargo, and US Bank, where investment representatives sell mutual funds and annuities to retail banking customers.

- 10The BLS projects 7% growth for personal financial advisors through 2034, with approximately 27,200 annual openings driven by retirement planning demand and the shift of investment services into bank branches.

Why This Comparison Matters

Limited License

Series 6 Product Scope

The Series 6 only authorizes sales of mutual funds, variable annuities, variable life insurance, and 529 plans. You cannot sell individual stocks, bonds, options, or ETFs — those require the Series 7.

$61,000

Median Salary (BLS)

Personal financial advisors holding a Series 6 license earn a median of approximately $61,000/year, with top performers at banks and insurance firms exceeding $86,000.

58% Pass Rate

Series 6 Is Deceptively Hard

Despite being a "limited" license, the Series 6 has a lower pass rate (~58%) than the SIE (~74%). The exam tests deep product knowledge on variable contracts, retirement plans, and tax regulations.

The SIE and Series 6 represent the most common entry path into financial services for bank employees and insurance professionals. While the Series 7 gets most of the attention in licensing discussions, the Series 6 quietly remains one of FINRA's most popular exams — particularly at large banks like JPMorgan Chase, Bank of America, Wells Fargo, and US Bank, where investment representatives sell mutual funds and annuities to retail banking customers.

The critical distinction most candidates fail to appreciate is the Series 6's product limitation. With a Series 6 license, you can sell mutual funds, variable annuities, variable life insurance, 529 college savings plans, and certain unit investment trusts — and nothing else. You cannot recommend or sell individual stocks, corporate bonds, municipal bonds, options, ETFs, or direct participation programs. This limitation defines the Series 6 career path: you will work primarily as a bank investment representative, an insurance agent offering variable products, or a mutual fund specialist. For professionals who operate exclusively in these product categories, the Series 6 is perfectly sufficient and significantly easier to obtain than the Series 7.

What surprises many candidates is the Series 6's 58% pass rate — substantially lower than both the SIE's 74% and the Series 7's 74%. The reason is deceptive simplicity: with only 50 scored questions and a narrow product focus, each question tests deeper, more granular knowledge. You must know mutual fund share class breakpoint schedules, variable annuity surrender charge structures, retirement plan contribution limits, and tax treatment nuances at a level of detail that the broader SIE only touches on. Do not let the "limited license" label lull you into under-preparing.

What Each Exam Covers

SIE Exam Topics

Pass Rate: ~74% first-time pass rate (FINRA data, 2023-2024)

Series 6 Exam Topics

Pass Rate: ~58% first-time pass rate (FINRA data, 2023-2024)

Salary & Income Comparison

SIE Credential Holder (Pre-License)

N/A — SIE alone is not a license

Median Annual Salary

Range: $40,000 - $55,000 (entry-level trainee positions)

ZipRecruiter, 2025; reflects trainee/associate roles that value SIE completion

The SIE is a prerequisite, not a standalone license. By itself it does not authorize you to conduct securities business or sell any investment products. However, listing SIE on your resume signals industry readiness and may help you secure a trainee position at a bank, insurance company, or broker-dealer where you will then take the Series 6 or Series 7.

Bank Investment Representative / Series 6 Licensed Agent

$61,000

Median Annual Salary

Range: $40,000 - $86,000

BLS Occupational Employment Statistics and Glassdoor data, 2024; reflects bank investment reps, insurance agents selling variable products, and mutual fund representatives

Compensation for Series 6 holders varies significantly by employer type. Bank investment representatives typically earn $50,000-$75,000 in base salary plus bonuses tied to assets gathered and products sold. Insurance agents selling variable annuities can earn $70,000-$100,000+ through commission structures that pay 4-7% of premium on annuity sales. Top-performing bank investment reps at large institutions like JPMorgan Chase, Bank of America, and Wells Fargo can exceed $90,000 with production bonuses.

The SIE alone does not unlock earning potential — it is a prerequisite, not a license. The Series 6 is where compensation begins, though it produces more modest earnings than the Series 7 due to its limited product scope. Series 6 holders working as bank investment representatives earn a median of approximately $61,000, with the range spanning $40,000 to $86,000 depending on institution size, geographic market, and production levels. Top-performing bank investment reps at major institutions can push past $90,000 when factoring in production bonuses and incentive compensation.

The compensation model for Series 6 holders differs from Series 7 stockbrokers. Rather than the grid-based commission structure of wirehouses, bank investment reps typically earn a base salary of $45,000-$65,000 plus quarterly or annual bonuses tied to assets gathered, products sold, and revenue generated. Insurance agents selling variable annuities through a Series 6 license often earn 4-7% commission on annuity premiums, which can produce significantly higher income — a single $500,000 annuity sale generates $20,000-$35,000 in commission. This is why many Series 6 holders gravitate toward annuity sales at insurance-affiliated broker-dealers. However, for those who want to break into the $100,000+ income range in securities sales, upgrading from a Series 6 to a Series 7 is the most common path, as it unlocks commission-based stock and bond transactions and access to wirehouse compensation grids.

Total Cost to Get Licensed

| Expense | SIE | Series 6 |

|---|---|---|

| Pre-Licensing Education | $0 (no pre-licensing course required, though $150-$400 for optional prep course recommended) | $100 - $350 (prep course: Kaplan $299, Achievable $129, ExamFX $149-$299, STC $299) |

| Exam Fee | $80 (FINRA) | $47 (FINRA) + $80 SIE if not already passed = $47-$127 |

| License Fee | N/A (SIE is not a license) | $147 (Series 63 typically required for state registration) |

| Background Check | N/A (no Form U4 filing for SIE alone) | $50 - $100 (fingerprinting and background check via Form U4) |

| Total Investment | $80 - $480 (exam fee + optional prep course) | $350 - $725 (SIE + Series 6 + Series 63 + prep courses + Form U4 processing) |

A Day in the Life

SIE Professional

A recent college graduate who passed the SIE last month arrives at a JPMorgan Chase branch for her final-round interview for a bank investment representative position. She confidently discusses mutual fund share classes, variable annuity structures, and retirement plan basics — topics she mastered for the SIE — impressing the branch investment manager. Over lunch, she reviews her notes on Series 6-specific topics like breakpoint schedules and 529 plan rules, knowing that if hired, she will need to pass the Series 6 within 90 days. By afternoon, she receives an offer: a $52,000 base salary plus quarterly production bonuses, with the firm covering her Series 6 and Series 63 exam fees and providing Kaplan study materials. She begins Series 6 prep that evening, leveraging the SIE knowledge she built just weeks earlier.

Series 6 Professional

A Series 6-licensed bank investment representative at Wells Fargo starts his day at 8:30 AM reviewing the morning's mutual fund performance reports and checking for any clients whose accounts triggered rebalancing alerts. At 9:15, he takes a referral from the personal banker — a couple in their 50s who just received a $200,000 inheritance and want to invest it wisely. He walks them through a diversified mutual fund portfolio using American Funds growth and income funds with Class A shares, applying the breakpoint discount on the large purchase. At 11:00, he calls a client who is turning 73 next month to discuss her required minimum distribution from her traditional IRA, calculating the amount and setting up systematic withdrawals into a money market fund. After lunch, he meets with a local business owner about establishing a SIMPLE IRA for his 12 employees, recommending a lineup of Vanguard index funds. At 3:00 PM, he conducts his weekly pipeline review with the branch manager: 4 pending 401(k) rollovers totaling $800,000, 2 variable annuity applications, and 6 new mutual fund accounts opened this week. He ends the day updating client records and preparing for tomorrow's retirement planning seminar for bank customers.

Career Paths & Progression

SIE Career Path

0 years

SIE Credential Holder (Job Seeker)

$0 (credential only)

0-1 years

Bank/Insurance Trainee (studying for Series 6)

$38K-$48K

Series 6 Career Path

0-2 years

Bank Investment Representative

$45K-$58K

2-5 years

Senior Investment Rep / Financial Consultant

$58K-$75K

5-10 years

Bank Branch Investment Manager / Annuity Specialist

$75K-$95K

10+ years

Regional Investment Director / Upgrades to Series 7 Path

$90K-$130K+

The SIE opens the door, but the Series 6 defines a specific career lane. After passing both exams, Series 6 holders typically follow one of three paths: (1) Bank investment representative — working within a retail bank branch at institutions like JPMorgan Chase, Bank of America, Wells Fargo, or US Bank, selling mutual funds and annuities to existing banking customers. This is the most common Series 6 career path, offering stable base salary plus production bonuses. (2) Insurance variable products agent — working at insurance companies or insurance-affiliated broker-dealers like Lincoln Financial, Pacific Life, or Prudential, selling variable annuities and variable life insurance. This path tends to be more commission-heavy and can produce higher income for strong salespeople. (3) Mutual fund company representative — working at firms like Fidelity, Vanguard, or T. Rowe Price in client-facing roles, helping investors select appropriate fund allocations.

A critical consideration for Series 6 holders is the upgrade question. Many professionals start with the Series 6 because their employer only requires it, then discover they want broader product authority. Upgrading to a Series 7 requires passing the full Series 7 exam — there is no abbreviated "top-off" option. This means studying an additional 80-120 hours for a separate 125-question exam covering stocks, bonds, options, and the full securities universe. For this reason, career advisors increasingly recommend starting with the Series 7 if there is any chance you will want broader authority later. However, if your career is firmly rooted in banking or insurance and you will only ever sell mutual funds and annuities, the Series 6 is the more efficient and focused credential.

Start preparing today:

Series 6 + State Registration: What Else Do You Need?

Benefits

- +The Series 6 + Series 63 combination is the standard for bank investment representatives — the Series 63 adds state-level securities registration required to transact business in your state

- +Adding the Series 63 (Uniform Securities Agent State Law Exam) is required in most states and costs only $147 with a relatively high pass rate — study for it immediately after the Series 6

- +Some firms require the Series 6 + Series 66 instead, which combines state securities registration with investment adviser representative authority — this allows you to charge advisory fees on assets under management

- +Series 6 holders can later add the Series 7 to upgrade from limited to full securities authority without losing their existing licenses

- +Holding both Series 6 and a life/health insurance license (state-level) creates a powerful combination for selling variable annuities and variable life insurance products that straddle the securities and insurance worlds

Considerations

- !The Series 6 is a LIMITED license — before pursuing it, seriously consider whether the Series 7 would be more valuable for your long-term career

- !If you later want to sell stocks, bonds, options, or ETFs, you must pass the full Series 7 exam — there is no "upgrade" or abbreviated test from the Series 6

- !Some employers (particularly wirehouses and full-service broker-dealers) do not accept the Series 6 at all — they require the Series 7 for all registered representatives

- !The Series 6 + Series 63 takes approximately 6-8 weeks total to complete (including SIE), compared to 10-14 weeks for the SIE + Series 7 + Series 66 path

The Verdict: The standard Series 6 career path is SIE → Series 6 → Series 63 (or Series 66), all completed within your firm's training window. This combination authorizes you to sell mutual funds, variable annuities, variable life insurance, and 529 plans in your registered states. If you work at a bank or insurance company that only requires the Series 6, this path is efficient and focused. However, if you have any ambition to sell individual securities or work at a wirehouse, start with the Series 7 instead — you will avoid the need to take a second major exam later. The key question to ask yourself: "Will I ever want to sell anything beyond mutual funds and annuities?" If the answer is yes or maybe, the Series 7 is the better investment of your time.

Job Outlook & Industry Trends

N/A (prerequisite exam)

SIE Job Growth (2024-2034)

7% (2024-2034, BLS — Personal Financial Advisors)

Series 6 Job Growth (2024-2034)

The BLS projects 7% growth for personal financial advisors through 2034, faster than the average for all occupations, with approximately 27,200 annual openings. For Series 6 holders specifically, demand is driven by two forces: (1) the continued shift of investment services into bank branches, where millions of retail banking customers are cross-sold mutual funds and annuities; and (2) the growing retirement planning market as approximately 10,000 baby boomers turn 65 every day, creating massive demand for retirement product specialists who can guide 401(k) rollovers, IRA contributions, and annuity purchases. Banks like JPMorgan Chase, Bank of America, and Wells Fargo continue to hire investment representatives at scale, and insurance companies are expanding their variable product distribution networks. However, candidates should note that the trend in the industry is moving toward broader licensing — many firms that previously accepted Series 6 only are now requiring or strongly encouraging the Series 7 for new hires.

Study Strategy & Tips

SIE Preparation

Foundational securities knowledge

- Complete an SIE prep course (Kaplan, Achievable, ExamFX, or similar)

- Study Products and Their Risks (44% of exam) first — equities, bonds, mutual funds, ETFs, options basics, and variable products

- Review Trading, Accounts, and Prohibited Activities (31%) — order types, account types, insider trading rules

- Pay special attention to mutual fund structures and variable annuity basics — these topics carry directly into the Series 6

- Take 3+ full-length practice exams, scoring 80%+ consistently before scheduling

Pass SIE + Begin Job Search

Pass SIE and secure firm sponsorship

- Schedule and pass the SIE exam

- Update resume with SIE credential

- Apply to bank investment programs, insurance firms, and broker-dealers that require the Series 6

- Begin reviewing Series 6 overlap material (mutual funds, variable contracts) while interviewing

Series 6 Deep Study

Intensive Series 6 preparation within firm training program

- Complete a Series 6 prep course — focus on the 36% Investment Company Products section

- Master mutual fund share classes (A, B, C), NAV calculations, breakpoints, rights of accumulation, and letter of intent

- Study variable annuity mechanics: separate accounts, accumulation/annuity phases, death benefits, surrender charges, and tax treatment

- Learn retirement plan rules: 401(k), traditional/Roth IRA, SEP, SIMPLE, 403(b), 529 — contribution limits, distributions, and rollovers

Series 6 Practice & Pass

Practice exams and pass

- Take 4-5 full-length timed practice exams (1 hour 30 minutes each)

- Score 80%+ consistently before scheduling — the 58% pass rate means thorough preparation is essential

- Focus on weak areas — most candidates need extra work on variable annuity tax treatment and retirement plan distribution rules

- Schedule and pass the Series 6 exam

Total Duration: 6-8 weeks for SIE + Series 6 (sequential study)

SIE Study Tips

- 1Focus 44% of your study time on Products and Their Risks — this is nearly half the exam. Know the characteristics, risks, and suitability of equities, debt securities, packaged products (mutual funds, ETFs), options, and alternative investments.

- 2Understand the difference between primary and secondary markets, the role of market makers, and how securities are issued (IPOs, secondary offerings). Capital Markets questions are straightforward if you understand the flow of money.

- 3Memorize key regulatory bodies and their jurisdictions: FINRA regulates broker-dealers, SEC oversees markets, MSRB governs municipal securities, and state regulators enforce blue sky laws.

- 4Take at least 3 full-length practice exams under timed conditions. The SIE tests breadth over depth — you need to recognize concepts quickly across a wide range of topics.

- 5If you plan to take the Series 6 after the SIE, pay extra attention to mutual fund structures, variable annuities, and investment company types — these topics carry over directly to the Series 6 exam.

Series 6 Study Tips

- 1Invest 36% of your study time in Investment Company Products — this is the largest section. Master mutual fund share classes (A, B, C), expense ratios, NAV calculations, front-end vs. back-end loads, breakpoints, rights of accumulation, and letter of intent provisions.

- 2Understand variable annuity mechanics thoroughly: separate accounts vs. general accounts, accumulation vs. annuity phases, death benefits, surrender charges, and the tax treatment of withdrawals (LIFO taxation of gains, 10% penalty before age 59 1/2).

- 3Study retirement plans deeply — 21% of the exam covers 401(k)s, traditional IRAs, Roth IRAs, SEP IRAs, SIMPLE IRAs, 403(b)s, and 529 plans. Know contribution limits, distribution rules, required minimum distributions (RMDs), and rollover rules.

- 4Do not underestimate the regulatory section (24%). Know SEC regulations, the Investment Company Act of 1940, prospectus delivery requirements, anti-money laundering (AML) rules, and suitability obligations under FINRA Rule 2111.

- 5Take at least 4-5 full-length practice exams. Despite having only 50 scored questions, the Series 6 has a lower pass rate (~58%) than the SIE because questions require detailed product knowledge and application — not just recognition.

Ready to Start Studying?

Free practice questions, study guides, and AI tutoring for the matching exam resources.

Frequently Asked Questions

QCan I take the Series 6 without the SIE?

No. Since FINRA restructured its exam system in October 2018, the SIE is a mandatory prerequisite for all representative-level exams, including the Series 6. You must pass the SIE before sitting for the Series 6. The only exception applies to individuals who passed certain legacy FINRA exams before 2018 that grandfathered their registration. For all new candidates entering the industry, the required path is SIE first, then Series 6 with firm sponsorship.

QWhat can I sell with a Series 6 that I cannot sell with just the SIE?

The SIE alone does not authorize you to sell anything — it is purely a knowledge prerequisite. With a Series 6 license, you can sell mutual funds (open-end investment company shares), variable annuities, variable life insurance policies, 529 college savings plans, and unit investment trusts that invest in mutual funds. However, the Series 6 does NOT authorize you to sell individual stocks, corporate bonds, municipal bonds, government bonds, options, ETFs, closed-end funds, or direct participation programs. If you need to sell any of those products, you must hold a Series 7 license instead.

QWhy is the Series 6 pass rate lower than the SIE pass rate?

The Series 6 has a roughly 58% pass rate compared to the SIE's 74%, which surprises many candidates. There are two main reasons. First, the Series 6 has only 50 scored questions covering a narrow product focus, which means each question drills deeper into specific product mechanics — mutual fund share class structures, variable annuity tax treatment, retirement plan contribution limits, and surrender charge schedules. Second, many candidates underestimate the Series 6 because it is labeled a "limited" license and allocate insufficient study time. The exam rewards granular product knowledge, not broad conceptual understanding, and the smaller question pool leaves less room for error.

QShould I get the Series 6 or Series 7?

It depends entirely on your career plans and your employer's requirements. Choose the Series 6 if you work at a bank or insurance company that only requires it, you plan to sell exclusively mutual funds and annuities, and you want the fastest path to licensure (30-50 hours of study vs 80-120 for Series 7). Choose the Series 7 if you want the broadest possible license, plan to sell stocks, bonds, options, or ETFs at any point, or work at a full-service broker-dealer or wirehouse. The critical consideration: if you take the Series 6 now and later decide you need the Series 7, you must pass the entire Series 7 exam from scratch — there is no credit or abbreviated path for existing Series 6 holders. Many career advisors recommend starting with the Series 7 to avoid this potential double-exam scenario.

QHow long does it take to get both the SIE and Series 6?

Most candidates complete both the SIE and Series 6 within 6-8 weeks of dedicated study. The SIE typically requires 40-60 hours of preparation over 2-3 weeks, and the Series 6 requires 30-50 hours over 2-3 weeks. Because there is meaningful content overlap — especially in mutual fund structures, variable products, and investment company regulations — studying for them sequentially is highly efficient. Most bank and insurance company training programs allow 90-120 days to complete all required licensing exams (SIE + Series 6 + Series 63). If you pass the SIE on your own before being hired, you can focus exclusively on the Series 6 and Series 63 during your training window, giving you a significant advantage.

QWhat is the total cost to get a Series 6 license?

The all-in cost for SIE + Series 6 + Series 63 (state registration) typically ranges from $350 to $725. This breaks down as: SIE exam fee ($80), Series 6 exam fee ($47), Series 63 exam fee ($147), prep course(s) ($100-$350), and Form U4 background check and fingerprinting ($50-$100). The good news is that most employers — especially banks like JPMorgan Chase, Bank of America, and Wells Fargo — cover all exam fees and provide proprietary or third-party study materials at no cost to the employee. In practice, many new hires pay $0 out of pocket for their licensing. Always ask about exam fee reimbursement and study material coverage during the interview process, as this is a standard benefit at most firms that require the Series 6.

10 free AI interactions per day

Free exam resources

Start Studying the Exact Exam

Use the comparison to choose a path, then move into the matching practice questions, study guide, and flashcards.

Related Exam Comparisons

Stay Updated

Get free exam tips and study guides delivered to your inbox.