Series 6 vs Series 66

The Series 6 and Series 66 serve fundamentally different purposes and, critically, are incompatible licensing paths. The Series 6 is a limited FINRA license that authorizes reps to sell only packaged products — mutual funds, variable annuities, variable life insurance, and 529 plans. The Series 66 is a NASAA state registration exam that combines the Series 63 (state agent registration) and Series 65 (investment adviser representative registration) into a single test. However, the Series 66 requires the Series 7 as a corequisite, and Series 6 holders do not have the Series 7. This means a Series 6 holder cannot take the Series 66 without first upgrading to the Series 7. Series 6 holders who need state registration take the Series 63 instead; those who want advisory capability must either upgrade to the Series 7 first (then take the Series 66) or take the Series 63 + Series 65 as separate exams.

Side-by-Side Comparison

| Feature | Series 6 | Series 66 |

|---|---|---|

| Full Name | Investment Company and Variable Contracts Products Representative Exam | Uniform Combined State Law Exam |

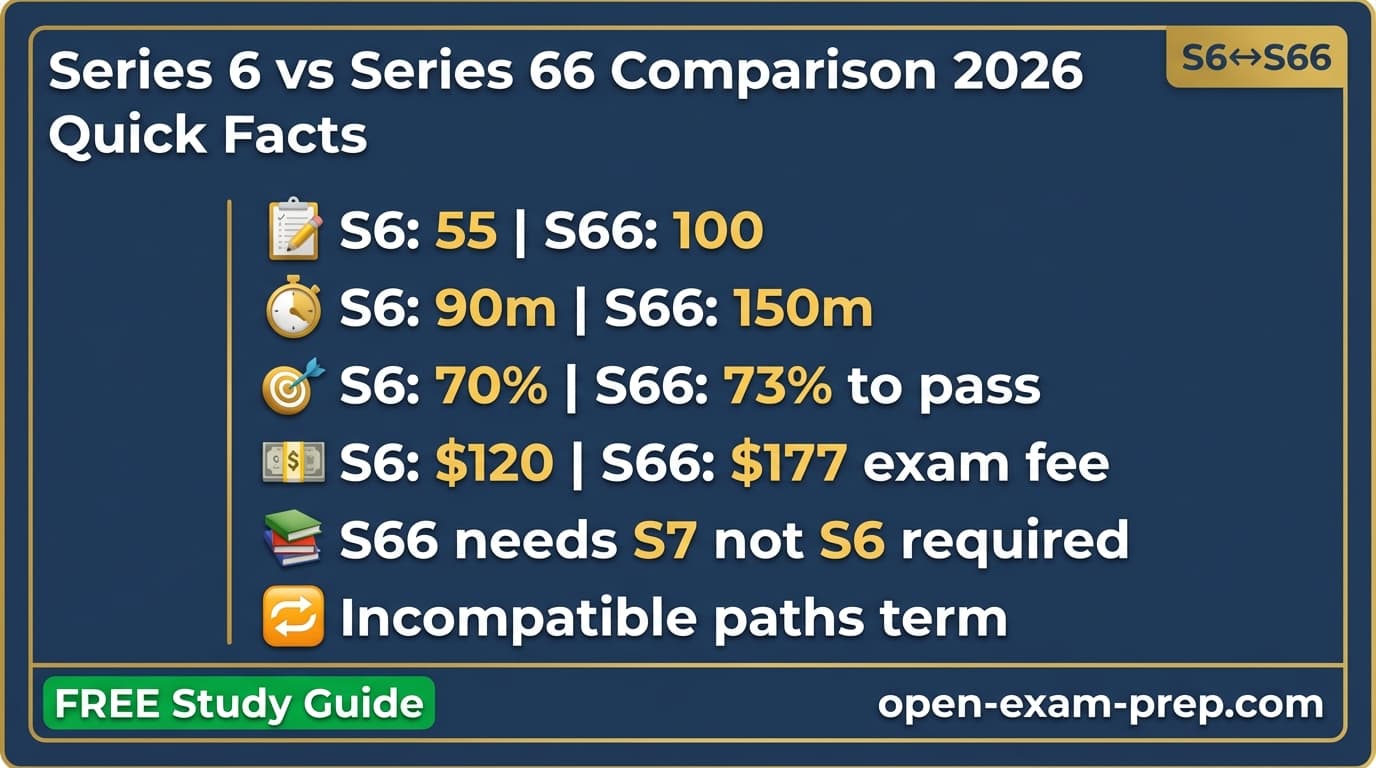

| Exam Cost | $47 | $177 |

| Passing Score | 70% (35 of 50 scored questions) | 73% (62 of 85 scored questions) |

| Questions | 55 (50 scored + 5 unscored) | 110 (100 scored + 10 unscored) |

| Time Limit | 1 hour 30 minutes | 2 hours 30 minutes |

| Study Time | 30 - 50 hours over 2 - 4 weeks | 50 - 70 hours over 3 - 5 weeks |

| Difficulty | Moderate | Moderate-Challenging |

| Prerequisites | SIE exam passed + sponsorship by a FINRA-member firm (Form U4) | REQUIRES the Series 7 (General Securities Representative) as a corequisite — you must pass or have passed the Series 7 to obtain Series 66 registration. SIE + firm sponsorship also required. |

| Exam Body | FINRA | NASAA (North American Securities Administrators Association) |

Key Differences

- 1The Series 6 is a FINRA product license that authorizes selling packaged products only (mutual funds, variable annuities, variable life, 529s). The Series 66 is a NASAA state registration exam that authorizes dual registration as both a securities agent and an investment adviser representative.

- 2The Series 66 requires the Series 7 as a corequisite — you cannot take or use the Series 66 without holding the Series 7. Series 6 holders do not have the Series 7, making these two exams fundamentally incompatible without an upgrade.

- 3Series 6 holders who need state-level securities agent registration take the Series 63 ($147), not the Series 66. The Series 66 is exclusively for Series 7 holders who want combined agent + adviser registration.

- 4The salary ceiling for Series 6 holders (~$61K median, capped around $80K-$95K) is dramatically lower than for Series 7 + 66 holders ($100K-$400K+ at wirehouses) because the limited product shelf restricts revenue opportunities.

- 5The Series 6 exam has 50 scored questions in 90 minutes and costs $47, while the Series 66 has 100 scored questions (85 scored per NASAA guidelines) in 150 minutes and costs $177 — reflecting the broader scope of the Series 66.

- 6The Series 6 is administered by FINRA; the Series 66 is developed by NASAA and administered at Prometric centers. They come from entirely different regulatory bodies with different mandates.

- 7Series 6 holders can sell products but cannot charge advisory fees. Series 66 holders (with the Series 7) can do both — earning commissions on product sales AND charging fees for investment advice, which is the dominant industry trend.

- 8The career trajectory is starkly different: Series 6 often leads to bank-channel or insurance-based roles with limited advancement, while Series 7 + 66 is the entry point for wirehouse advisor careers with six-figure and seven-figure earning potential.

What Each Exam Allows You To Do

Series 6

- Sell mutual funds (open-end investment company shares)

- Sell variable annuities and variable life insurance contracts

- Sell 529 college savings plans

- Sell unit investment trusts (UITs)

- Collect commissions on packaged product sales at banks, insurance agencies, and limited broker-dealers

Series 66

- Register as a securities agent in your state (equivalent to Series 63 functionality)

- Register as an investment adviser representative (IAR) in your state (equivalent to Series 65 functionality)

- Provide investment advice for a fee in addition to earning commissions on trades

- Operate as a dual-registered representative: sell securities on a commission basis AND manage fee-based advisory accounts

- Work at dual-registered firms (broker-dealer + RIA) — the fastest-growing segment of the advisory industry

Who Should Take Each Exam?

Take the Series 6 if you...

- →Bank-based investment representatives selling mutual funds alongside deposit products

- →Insurance agents adding variable annuity and variable life insurance sales to their practice

- →Reps at limited broker-dealers that only sell packaged products

- →Professionals who want a quicker, cheaper entry point into securities sales with a narrower product scope

Take the Series 66 if you...

- →Series 7 holders at wirehouses who need state registration as both agent and adviser

- →Financial advisors building fee-based practices at dual-registered firms

- →Registered reps who want to charge advisory fees in addition to earning commissions

- →Anyone pursuing the full-service advisor career path (Series 7 + Series 66 is the industry standard)

Which Should You Take First?

This is not a "which to take first" question — it is a "which path to choose" decision, because these exams belong to incompatible licensing tracks. If you already hold the Series 6, you have three options for expanding your capabilities: (1) **Upgrade to Series 7 first, then take the Series 66.** This is the most career-enhancing path but requires your firm to sponsor you for the Series 7, which means transitioning from a limited to a full-service role. (2) **Take the Series 63 for state agent registration.** This is the standard path for Series 6 holders who just need to register in their state to sell mutual funds and variable products. (3) **Take the Series 63 + Series 65 separately.** This gives you state agent registration (63) plus investment adviser representative registration (65) without needing the Series 7, though your product authority remains limited to Series 6 products. For new entrants who have not yet chosen a path, the Series 7 + Series 66 combination is overwhelmingly the better long-term career investment. The Series 6 path only makes sense if your employer specifically requires it and you are confident you will not want broader product authority in the future.

At a Glance: Series 6 vs Series 66

Exam Cost

$47

Series 6

$177

Series 66

Pass Rate

~58%

Series 6

~73%

Series 66

Study Time

30-50 hrs

Series 6

50-70 hrs

Series 66

Earning Potential

~$61K median

Series 6

$100K-$400K+

Series 66

Series 6

Reps selling only mutual funds, variable annuities, variable life insurance, and 529 plans at banks, insurance companies, or limited broker-dealers

Series 66

Financial advisors and registered reps who already hold the Series 7 and need dual state registration as both a securities agent and an investment adviser representative

Start preparing today:

Key Facts: Series 6 vs Series 66

- 1The Series 66 requires the Series 7 as a corequisite, meaning Series 6 holders cannot take the Series 66 without first upgrading to the Series 7 — these are fundamentally incompatible licensing paths.

- 2The Series 6 is a limited FINRA license ($47, 50 scored questions, 90 minutes) authorizing sales of only mutual funds, variable annuities, variable life insurance, and 529 plans, while the Series 66 is a NASAA state registration exam ($177, 100 questions, 150 minutes) that enables dual registration as both a securities agent and investment adviser representative.

- 3Series 6 holders who need state registration take the Series 63 ($147), not the Series 66. The Series 66 combines the Series 63 + Series 65 into one exam but is exclusively available to Series 7 holders.

- 4The median salary for Series 6 holders is approximately $61,600 per year with a ceiling around $80K-$95K, compared to $100,000-$400,000+ for Series 7 + 66 holders at wirehouses, according to BLS May 2024 data and industry compensation surveys.

- 5The Series 6 has a first-time pass rate of approximately 58% (FINRA, 2023-2024), while the Series 66 has a higher pass rate of approximately 73% (NASAA, 2023-2024) despite being a longer and more complex exam.

- 6Upgrading from Series 6 to Series 7 costs $245 in exam fees, plus $177 for the Series 66 — a total of $422 that typically pays for itself within the first week of higher compensation.

- 7The Series 66 exam is 45% focused on state securities law and regulation (Uniform Securities Act), making it fundamentally different from the product-focused Series 6 exam, which is 62% about investment recommendations and product suitability.

- 8An estimated 30-40% of financial advisors will retire by 2030, creating significant opportunities for new entrants who hold the Series 7 + 66 combination — but limited opportunities for those holding only the Series 6.

- 9Series 6 holders who want advisory capability without taking the Series 7 can take the Series 65 as a standalone exam ($187), but their product authority remains limited to mutual funds, variable annuities, variable life, and 529 plans.

- 10The total cost to become fully licensed through the Series 6 path (SIE + Series 6 + Series 63) ranges from $425-$725, compared to $850-$1,400 for the Series 7 + 66 path — a modest cost difference that produces a dramatically different career trajectory.

Why This Comparison Matters

Incompatible

These Paths Do Not Connect

The Series 66 requires the Series 7 as a corequisite. Series 6 holders do not have the Series 7, so they cannot sit for the Series 66 exam without first upgrading their license.

$61K vs $100K+

Massive Salary Gap

Series 6 holders earn a median of ~$61K selling limited products. Series 7 + 66 holders at wirehouses earn $100K-$400K+ with access to the full product shelf and advisory fees.

S7 + S66

The Industry Standard

Over 80% of wirehouse training programs require the Series 7 + Series 66 combination. The Series 6 path is increasingly viewed as a career-limiting credential.

This is one of the most misunderstood comparisons in securities licensing, and the confusion costs people real career time. Many aspiring financial professionals assume that because both exams exist within the securities licensing ecosystem, they can be combined freely. They cannot. The Series 66 has an absolute, non-negotiable corequisite: you must hold the Series 7 to use the Series 66 registration. Since the Series 6 is a different, more limited license than the Series 7, these paths simply do not connect.

The root issue is that the Series 6 was designed for a narrower role: selling packaged investment products at banks and insurance companies. It was never intended as a stepping stone to full-service advisory work. The Series 66, by contrast, was created as a companion to the Series 7 — giving full-service representatives the ability to also register as investment adviser representatives in their states. Pairing the Series 66 with the Series 6 would create an internally contradictory credential: advisory authority without the underlying product knowledge to exercise it.

If you are a Series 6 holder reading this, the critical question is whether your career ambitions have outgrown your license. The $61K median salary for Series 6 roles versus the $100K-$400K+ potential for Series 7 + 66 holders is not just a statistic — it reflects a fundamental structural difference in earning capacity. Upgrading to the Series 7 is the single highest-ROI career move available to you in the securities industry.

What Each Exam Covers

Series 6 Exam Topics

Pass Rate: ~58% first-time pass rate (FINRA data, 2023-2024)

Series 66 Exam Topics

Pass Rate: ~73% first-time pass rate (NASAA data, 2023-2024)

Salary & Income Comparison

Investment Company Products Representative / Insurance Sales Agent

$61,600

Median Annual Salary

Range: $35,000 - $95,000

BLS Occupational Employment Statistics, May 2024 (SOC 41-3021 for Insurance Sales Agents); ZipRecruiter and Glassdoor 2024 data for mutual fund/bank rep roles

Series 6 compensation is structurally limited because you can only sell packaged products. Top earners typically work in bank channels where mutual fund sales volume is high, or in insurance firms selling variable annuities with generous trail commissions. However, the ceiling is far lower than full-service brokerage: most Series 6 reps plateau at $80,000-$95,000 even with strong performance, because they cannot offer individual stocks, bonds, options, or fee-based advisory services.

Financial Advisor / Registered Representative with Dual Registration (Series 7 + 66)

$78,140 (BLS baseline); $100,000-$200,000 typical for advisors with 3-5 years experience

Median Annual Salary

Range: $47,080 - $400,000+

BLS Occupational Employment Statistics, May 2024 (SOC 41-3031); wirehouse compensation grids and industry surveys from Cerulli Associates and InvestmentNews, 2024

The Series 66 itself does not independently drive salary — its value is unlocked in combination with the Series 7. Together, these licenses give advisors the ability to earn both commission-based and fee-based revenue. Wirehouse advisors at Morgan Stanley, Merrill Lynch, UBS, and Wells Fargo earn **35-51% of revenue produced** via grid compensation. An advisor generating $1M in annual revenue earns $350,000-$510,000. The fee-based advisory component (enabled by the Series 66) is increasingly the dominant revenue stream, as the industry shifts from transactional to recurring-fee models.

The compensation gap between Series 6 holders and Series 7 + 66 holders is among the largest in the financial services licensing landscape. According to BLS May 2024 data and industry compensation surveys, Series 6 representatives earn a median of approximately $61,600 per year, with most earning between $35,000 and $95,000. Even the highest-performing Series 6 reps plateau below $100K because their product shelf is limited to mutual funds, variable annuities, variable life insurance, and 529 plans.

Series 7 + 66 holders operate in a completely different economic tier. BLS reports a median of $78,140 for securities sales agents (SOC 41-3031), but this figure blends entry-level reps with seasoned advisors and significantly understates top-earner compensation. At wirehouses like Morgan Stanley, Merrill Lynch, UBS, and Wells Fargo, advisors earn 35-51% of the revenue they generate through a grid-based payout system. An advisor producing $500,000 in annual revenue earns $175,000-$255,000; at $1M in revenue, the take-home reaches $350,000-$510,000. Independent broker-dealer reps keep 80-95% of gross revenue while covering their own overhead.

The Series 66 specifically amplifies earning potential by unlocking fee-based advisory revenue. As the industry shifts from commission-based transactions to recurring advisory fees (typically 0.75%-1.25% of assets under management), the advisory capability enabled by the Series 66 has become the primary revenue driver for most advisors. An advisor managing $50M in client assets at a 1% fee generates $500,000 in annual recurring revenue — a stable, growing income stream that Series 6 holders simply cannot access.

Total Cost to Get Licensed

| Expense | Series 6 | Series 66 |

|---|---|---|

| Pre-Licensing Education | $100 - $350 (prep course: Kaplan $269, Achievable $149, STC $150-$300) | $300 - $800 (prep courses for both Series 7 and Series 66) |

| Exam Fee | $47 (FINRA) + $80 SIE = $127 | $245 (Series 7, FINRA) + $177 (Series 66, NASAA) + $80 (SIE) = $502 |

| License Fee | $147 (Series 63 for state registration, almost always required) | Included in Series 66 fee (dual registration as agent + adviser) |

| Background Check | $50 - $100 (fingerprinting and Form U4 processing) | $50 - $100 (fingerprinting and Form U4 processing) |

| Total Investment | $425 - $725 (SIE + Series 6 + Series 63 + prep courses + background check) | $850 - $1,400 (SIE + Series 7 + Series 66 + prep courses + background check) |

A Day in the Life

Series 6 Professional

A Series 6 representative at a regional bank starts her day at 8:30 AM reviewing a list of bank customers whose CDs are maturing this week. At 9:00 AM, she meets with a retired couple who have $150,000 in a maturing 12-month CD and discusses mutual fund options that offer higher potential returns with moderate risk — she recommends a balanced fund and a short-term bond fund. At 10:30, she reviews a variable annuity application for a client in her 50s, ensuring the surrender schedule and death benefit features match the client’s retirement timeline. Over lunch, she attends a wholesaler presentation on a new target-date fund series. In the afternoon, she calls five clients whose 529 plan contributions are below the annual gift tax exclusion limit, suggesting they maximize contributions before year-end. She ends the day completing compliance paperwork for two mutual fund switches that require supervisory approval. Her total product recommendations for the day: mutual funds, a variable annuity, and 529 plans — the full extent of what her Series 6 license allows.

Series 66 Professional

A Series 7 + 66 financial advisor at a wirehouse arrives at 7:15 AM and reviews overnight market movements, flagging two client portfolios that need rebalancing after a sector rotation. At 8:30, she meets with a business owner couple exploring a comprehensive financial plan: she discusses asset allocation across individual stocks, bonds, and ETFs in their brokerage account, reviews their 401(k) plan options, analyzes whether to convert a traditional IRA to a Roth, and evaluates covered call strategies on concentrated stock positions — all advice she can provide because her Series 7 covers the full product shelf and her Series 66 authorizes her to charge a 1% advisory fee on assets under management. At 10:30, she presents a retirement income plan to a new prospect with $2M in investable assets, recommending a mix of dividend stocks, municipal bonds for tax efficiency, and a fixed indexed annuity for guaranteed income. After lunch, she leads a seminar for 20 pre-retirees on Social Security optimization strategies. By 3:00 PM, she is executing trades and reviewing a transfer of assets from a competitor firm. Her fee-based accounts generate $450,000 in annual recurring revenue, supplemented by commission income on new product placements.

Career Paths & Progression

Series 6 Career Path

0-2 years

Bank Investment Representative / Mutual Fund Rep

$35K-$50K

3-5 years

Senior Bank Investment Specialist / Variable Annuity Rep

$55K-$75K

5-10 years

Branch Investment Manager / Senior Insurance Rep

$75K-$95K

10+ years

Regional Sales Manager (Bank Channel)

$90K-$120K

Series 66 Career Path

0-2 years

Wirehouse Trainee / Associate Financial Advisor (S7 + S66)

$50K-$80K base

3-5 years

Financial Advisor / Wealth Advisor

$100K-$200K

5-10 years

Senior Vice President / Senior Financial Advisor

$200K-$400K

10+ years

Managing Director / Private Wealth Advisor

$400K-$800K+

The Series 6 career path is structurally constrained by product limitations. Most Series 6 holders work in one of three channels: (1) Bank investment programs — selling mutual funds and annuities alongside traditional banking products to bank customers. These roles pay a base salary plus commissions, with total compensation typically ranging from $45,000-$85,000. (2) Insurance companies — selling variable annuities and variable life insurance, often as an add-on to a property/casualty or life insurance practice. (3) Limited broker-dealers — small firms that only transact in packaged products. In all three channels, the revenue ceiling is constrained because you cannot sell individual securities, recommend asset allocation across the full product shelf, or charge advisory fees.

The Series 7 + 66 combination opens entirely different career trajectories. Wirehouse advisors at Morgan Stanley, Merrill Lynch, UBS, and Wells Fargo follow structured training programs (18-24 months) and transition to grid-based compensation, where earning potential scales linearly with client assets and revenue production. Independent broker-dealer reps at firms like LPL Financial, Raymond James, and Cetera keep 80-95% of revenue and run their own practices. Hybrid RIA advisors at dual-registered firms combine brokerage and advisory services, earning both transaction-based and fee-based revenue. The common denominator across all three paths: the Series 7 provides the full product shelf, and the Series 66 provides the advisory authority that increasingly drives revenue in the modern wealth management industry.

For Series 6 holders considering an upgrade, the math is compelling. The cost of taking the Series 7 exam ($245) and Series 66 exam ($177) totals $422 in exam fees. The potential salary increase from ~$61K to $100K+ represents a $39,000+ annual gain — meaning the upgrade pays for itself within the first week of the higher salary.

Start preparing today:

Upgrading from Series 6: Your Options for Expanding Capabilities

Benefits

- +Upgrading from Series 6 to Series 7 unlocks the entire securities product shelf — individual stocks, bonds, options, ETFs, and direct participation programs — dramatically increasing your revenue potential and client service capability.

- +Adding the Series 66 after the Series 7 provides dual state registration (agent + adviser) in a single exam, which is more efficient than taking the Series 63 and Series 65 separately (two exams, two fees, two study periods).

- +The Series 7 + 66 combination is the recognized industry standard at wirehouses and major independent broker-dealers — it signals that you are fully qualified to both transact in securities and provide investment advice for fees.

- +Fee-based advisory revenue (enabled by the Series 66) creates a recurring, scalable income stream that is more stable than commission-based revenue alone — this is the direction the entire wealth management industry is moving.

- +Series 6 holders who upgrade to Series 7 often find the exam easier than expected because 50-60% of Series 7 content overlaps with or builds upon Series 6 material, particularly in mutual funds, variable products, and suitability.

Considerations

- !Upgrading to Series 7 requires your firm to sponsor you, which may mean transitioning to a different role or department within your firm — or changing firms entirely to one that supports full-service representatives.

- !The Series 7 requires significantly more study time (80-120 hours) and covers complex topics like options strategies and bond mathematics that go well beyond Series 6 content.

- !Some states do not accept the Series 66 and require the Series 63 + Series 65 taken separately — verify requirements with your state securities regulator before choosing your path.

- !If you do not want to take the Series 7, you can still gain advisory capability by taking the Series 65 (standalone investment adviser representative exam) in addition to the Series 63 — but your product authority remains limited to Series 6 products.

The Verdict: For Series 6 holders with career ambitions beyond bank-channel or insurance-based product sales, the single best move is to upgrade to the Series 7 and then take the Series 66. The combined exam fees total approximately $422 ($245 for the Series 7 + $177 for the Series 66), which is trivial compared to the $39,000+ annual salary increase this upgrade typically produces. If upgrading to the Series 7 is not feasible in the near term, take the Series 63 for immediate state registration and plan the Series 7 upgrade as a medium-term career goal. The Series 6 path is viable for some roles, but treating it as a permanent credential means accepting a permanently lower ceiling.

Job Outlook & Industry Trends

6% (2024-2034, BLS — Insurance Sales Agents, SOC 41-3021)

Series 6 Job Growth (2024-2034)

3% (2024-2034, BLS — Securities Sales Agents, SOC 41-3031)

Series 66 Job Growth (2024-2034)

The job outlook for both paths reflects broader industry trends, but the nature of the demand is very different. Series 6 roles are growing at 6% (BLS) due to continued demand for insurance and annuity products as baby boomers manage retirement income, but this growth is concentrated in lower-paying bank and insurance channels. Series 7 + 66 roles show 3% growth with approximately 38,100 annual openings, driven by retirements and the ongoing shift to fee-based advisory. The critical dynamic is the industry’s migration from commission-based product sales (where Series 6 lives) to fee-based advice (where Series 66 enables revenue). An estimated 30-40% of financial advisors will retire by 2030, creating unprecedented opportunities for young professionals who enter with the full Series 7 + 66 credential. Series 6 holders who do not upgrade risk being left in a shrinking segment of the industry.

Study Strategy & Tips

Assessment and Path Selection

Determine your licensing path based on current credentials and career goals

- If you have no licenses yet: choose between the Series 6 path (limited) or Series 7 path (full-service). The Series 7 path is recommended for long-term career growth.

- If you hold Series 6 and want advisory capability: decide between upgrading to Series 7 + 66 (best ROI) or taking Series 63 + 65 separately (no Series 7 required).

- Confirm your firm’s sponsorship willingness and training timeline — upgrading to Series 7 requires firm support.

- Select and purchase prep materials: Kaplan, Achievable, Securities Training Corporation (STC), or Knopman Marks.

Series 6 Preparation (if taking this path)

Master packaged products and suitability

- Study mutual fund mechanics: NAV calculation, share classes (A, B, C), breakpoints, rights of accumulation, 12b-1 fees, and redemption fees.

- Learn variable annuity and variable life insurance: accumulation/annuitization phases, separate accounts, surrender charges, 1035 exchanges, tax treatment.

- Review suitability requirements, customer account types, and FINRA rules governing packaged product sales.

- Take 3+ full-length practice exams, targeting 80%+ before scheduling.

Series 7 Preparation (if upgrading or choosing the full-service path)

Comprehensive securities knowledge including equities, debt, options, and suitability

- Leverage existing Series 6 knowledge as a foundation — expand from packaged products to individual stocks, bonds, options, and direct participation programs.

- Master options: four basic positions, breakeven formulas, max gain/loss, spreads, straddles, and combinations (this is where most candidates struggle).

- Study bond pricing and yields: current yield, YTM, YTC, discount vs. premium bonds, duration, and tax-equivalent yield calculations.

- Take 5-8 full-length timed practice exams (3 hours 45 minutes each). Score 80%+ consistently before scheduling.

Series 66 Preparation

State securities law, fiduciary standards, and advisory regulations

- Study the Uniform Securities Act: registration requirements for agents, broker-dealers, investment advisers, and securities. This is 45% of the exam.

- Master fiduciary duty concepts: fiduciary vs. suitability standard, prohibited practices, disclosure obligations, and conflicts of interest.

- Learn Form ADV requirements, advisory contract rules, custody regulations, and the definition/exemptions for investment advisers.

- Review investment recommendations and portfolio strategies: asset allocation, risk-adjusted returns, retirement planning, and tax considerations.

- Take 4-5 full-length practice exams targeting 80%+ before scheduling.

Total Duration: 8-14 weeks (varies by starting point: new candidate vs. Series 6 holder upgrading)

Series 6 Study Tips

- 1Focus 62% of your study time on product knowledge and suitability — this is the overwhelming majority of the exam. Know the differences between Class A, B, and C mutual fund shares, breakpoints, rights of accumulation, letters of intent, and when each share class is most suitable.

- 2Master variable annuity mechanics: accumulation vs. annuitization phase, death benefits, surrender charges, 1035 exchanges, and the tax treatment of withdrawals (LIFO for gains, then return of cost basis). Variable annuity questions are a major exam component.

- 3Understand 529 plan features thoroughly: qualified expenses, gift tax treatment, state tax deductions, rollovers, and the impact on financial aid. FINRA has increased 529 content in recent years.

- 4Learn the regulatory framework for packaged products: Investment Company Act of 1940, prospectus delivery requirements, NAV calculation (forward pricing), and the difference between open-end funds, closed-end funds, and UITs.

- 5Take at least 3 full-length practice exams. The Series 6 is short (50 scored questions in 90 minutes) so pacing is rarely an issue, but the questions can be tricky — especially suitability scenarios that require you to weigh multiple factors.

Series 66 Study Tips

- 1Dedicate 45% of your study time to state securities law and regulation — this is nearly half the exam. Understand the Uniform Securities Act, registration requirements for agents, broker-dealers, and investment advisers, and the differences between federal and state regulatory authority.

- 2Master the fiduciary standard vs. suitability standard distinction. The Series 66 tests your understanding of when you act as a broker (suitability standard) vs. when you act as an adviser (fiduciary standard). Know the key differences, prohibited practices under each, and how dual registration creates overlapping obligations.

- 3Study investment advisory regulations in depth: Form ADV Parts 1 and 2, advisory fee structures, custody rules, brochure delivery requirements, and the definition of “investment adviser” under both federal and state law (the exclusions and exemptions are heavily tested).

- 4Review client recommendation strategies: asset allocation, modern portfolio theory basics, risk-adjusted returns, tax-loss harvesting, and retirement account rules (IRA contributions, RMDs, Roth conversions). The exam blends regulatory knowledge with practical advisory skills.

- 5Take at least 4-5 full-length practice exams under timed conditions. The Series 66 covers a wide range of topics at moderate depth, and many candidates underestimate the state law component. Score 80%+ consistently before scheduling.

Ready to Start Studying?

Free practice questions, study guides, and AI tutoring for the matching exam resources.

Frequently Asked Questions

QCan I take the Series 66 if I only have the Series 6?

No. The Series 66 has an absolute corequisite: you must hold the Series 7 (General Securities Representative) license. The Series 6 is a different, more limited license that does not satisfy this requirement. If you hold the Series 6 and want state registration, the standard path is the Series 63 (Uniform Securities Agent State Law Exam), which costs $147 and covers state-level securities regulations. If you want advisory capability (the ability to charge fees for investment advice), you will need to either upgrade to the Series 7 first and then take the Series 66, or take the Series 65 as a standalone exam without the Series 7.

QWhat is the fastest way for a Series 6 holder to get investment adviser representative (IAR) registration?

The fastest path is to take the Series 65 (Uniform Investment Adviser Law Exam) as a standalone exam. The Series 65 costs $187, has 130 questions (100 scored plus 10 pretest) in 180 minutes, and does not require the Series 7. Passing it qualifies you as an investment adviser representative in your state, allowing you to charge fees for investment advice. However, your product authority remains limited to Series 6 products (mutual funds, variable annuities, variable life, 529 plans). For the broadest career capability, upgrading to the Series 7 and then taking the Series 66 is the better long-term investment, even though it requires more study time and firm sponsorship for the Series 7.

QWhy is the Series 6 pass rate (~58%) lower than the Series 66 pass rate (~73%)?

This counterintuitive result likely reflects the candidate populations rather than exam difficulty. Series 66 candidates have already passed the more rigorous Series 7 exam, meaning they enter the Series 66 with strong study habits, test-taking skills, and foundational knowledge. Series 6 candidates are often newer to the securities industry and may be taking their first FINRA exam beyond the SIE. Additionally, Series 6 candidates are frequently studying while working full-time in bank or insurance roles, with less dedicated study time than wirehouse trainees who often have structured training programs with protected study periods. The Series 66 is not an easier exam — it is a longer test covering a broader range of material — but its candidates tend to be better prepared.

QIs it worth upgrading from Series 6 to Series 7?

For most professionals, upgrading from the Series 6 to the Series 7 is the single highest-ROI career move in the securities industry. The median salary gap is approximately **$39,000+ per year** ($61K for Series 6 roles vs. $100K+ for Series 7 roles with a few years of experience), and the long-term ceiling is dramatically higher: Series 7 + 66 holders at wirehouses routinely earn $200K-$400K+ with established client books, compared to the $80K-$95K ceiling for most Series 6 roles. The upgrade costs $245 in exam fees and requires 80-120 hours of additional study, but approximately 50-60% of Series 7 content overlaps with or builds on Series 6 material. The primary challenge is not the exam itself but securing firm sponsorship for the Series 7, which may require a role change or firm transition.

QWhat exams does a Series 6 holder need for complete state registration?

A Series 6 holder needs the Series 63 (Uniform Securities Agent State Law Exam) for basic state registration to sell packaged investment products. The Series 63 costs $147, has 60 questions (50 scored) in 75 minutes, and covers state securities regulations under the Uniform Securities Act. If the Series 6 holder also wants to act as an investment adviser representative (to charge advisory fees), they additionally need the Series 65, which costs $187 and has 130 questions in 180 minutes. Note that the Series 6 + Series 63 + Series 65 combination achieves similar state-level authority as the Series 7 + Series 66, except the product authority remains limited to Series 6 products. This is why the upgrade to Series 7 + 66 is generally recommended — it provides both full product authority and dual state registration in a more efficient package.

QCan I hold both the Series 6 and Series 7 at the same time?

Yes. If you currently hold the Series 6 and pass the Series 7, you will hold both licenses simultaneously. In practice, the Series 7 makes the Series 6 redundant because the Series 7 authorizes everything the Series 6 does and much more — individual stocks, bonds, options, ETFs, direct participation programs, and all packaged products. Many firms will have you take the Series 7 as an upgrade rather than a replacement, so both registrations appear on your CRD record. Once you have the Series 7, you can then take the Series 66 for dual state registration as a securities agent and investment adviser representative. The full upgrade path is: keep your Series 6, add the Series 7, then add the Series 66 — giving you the maximum licensing authority available to a registered representative.

10 free AI interactions per day

Free exam resources

Start Studying the Exact Exam

Use the comparison to choose a path, then move into the matching practice questions, study guide, and flashcards.

Related Exam Comparisons

Stay Updated

Get free exam tips and study guides delivered to your inbox.