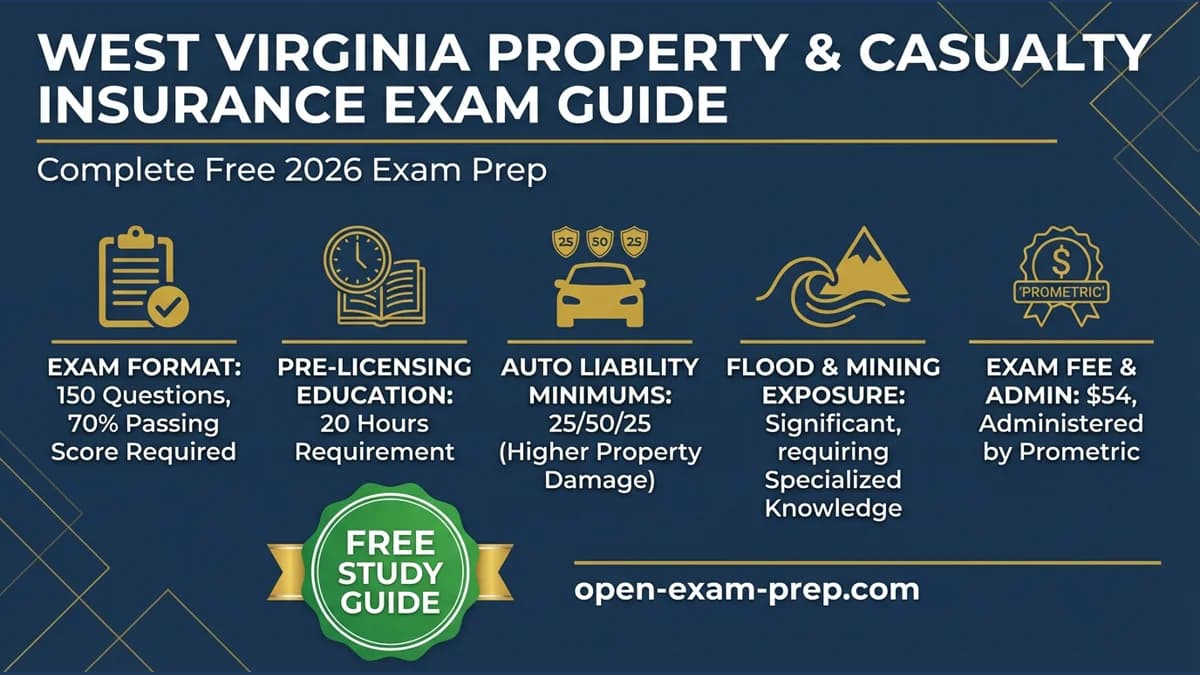

West Virginia Property & Casualty Insurance License Exam Overview

The West Virginia Property & Casualty Insurance License Exam is administered by Pearson VUE on behalf of the West Virginia Offices of the Insurance Commissioner (OIC). West Virginia's unique geography and economy—including coal mining, natural gas, and manufacturing—create specialized insurance needs that show up on the state-specific portion of the exam.

Passing this exam qualifies you to sell property insurance, auto insurance, liability coverage, and related products throughout West Virginia—a state with approximately 1.8 million residents, significant flood exposure, and an energy sector that creates substantial commercial P&C insurance demand.

Exam Format at a Glance (Combined P&C)

| Component | Details |

|---|---|

| Exam Code | 03 (Property & Casualty combined) |

| Scored Questions | 140 multiple-choice |

| Pretest Questions | 18 (unscored, mixed in) |

| Total Questions | 158 |

| Time Limit | 210 minutes (3 hours 30 minutes) |

| Passing Score | 70 scaled score |

| Testing Vendor | Pearson VUE |

| Exam Fee | $84 (paid at reservation) |

| Pre-licensing Education | 40 hours combined (20 Property + 20 Casualty) |

The exam code "03" is the combined Property & Casualty appointment. The older "InsWV-PC03" label that some outdated prep articles still show is not the code Pearson VUE uses when you register.

Separate Line Exams vs. One Combined Exam

West Virginia offers three Pearson VUE appointments for property/casualty licensing, and candidates often misunderstand the choice. You can take the lines separately or together in a single appointment:

| Exam | Code | Scored Questions | Pretest | Total | Time | Fee |

|---|---|---|---|---|---|---|

| Property only | 30 | 80 | 15 | 95 | 2 hours | $84 |

| Casualty only | 40 | 80 | 15 | 95 | 2 hours | $84 |

| Property & Casualty combined | 03 | 140 | 18 | 158 | 3 hrs 30 min | $84 |

Each exam costs $84 per appointment, so taking the two lines separately costs $168 total versus $84 for the combined exam. Most candidates who want both lines take the combined exam (code 03) in one sitting. If you pass one line and fail the other, you only retake the failed line.

Official Combined P&C Content Outline and Weights

The Pearson VUE content outline (effective June 16, 2026) splits the combined P&C exam into three blocks. The West Virginia state-law block is the single largest section, so do not treat state law as a side topic.

| Content Block | Scored Questions | % of Exam |

|---|---|---|

| Casualty Insurance — Types of Policies, Bonds, and Related Terms | 23 | 16% |

| Casualty Insurance — Insurance Terms and Related Concepts | 15 | 11% |

| Casualty Insurance — Policy Provisions | 12 | 9% |

| Property Insurance — Types of Property Policies | 22 | 16% |

| Property Insurance — Property Insurance Terms and Related Concepts | 15 | 11% |

| Property Insurance — Property Policy Provisions and Contract Law | 13 | 9% |

| West Virginia Laws and Rules Pertinent to Property & Casualty Insurance | 40 | 29% |

| Total scored | 140 | 100% |

If you take Property only (code 30) or Casualty only (code 40), the state-law block changes: Property-only adds 30 scored West Virginia property-specific law questions (38% of that exam), and Casualty-only adds 30 scored West Virginia casualty-specific law questions (38% of that exam).

Fee Table: Full Cost to Get Licensed

| Item | Cost | Who Sets It |

|---|---|---|

| Prelicensing course (40 hrs combined) | ~$140–$200 | Approved provider |

| Pearson VUE exam fee | $84 per appointment | Pearson VUE |

| Fingerprinting (IdentoGo) | $45.75 | IdentoGo / WV State Police |

| Resident producer license application | $50 | WV OIC / NIPR |

| License renewal (every 2 years) | $50 | WV OIC / NIPR |

| Continuing education (24 hrs/2 yrs) | Varies by provider | Approved CE provider |

Your total out-of-pocket to reach an active resident P&C license typically runs about $320–$380 before prelicensing course sales tax, depending on the provider you choose. Fingerprinting and exam fees are set by outside vendors and can change; confirm the current amount on the WV OIC Licensing page before you schedule.

Why Get P&C Licensed in West Virginia?

- Growing market — Energy sector and infrastructure growth

- Unique exposures — Flood, mining, and mountain terrain

- Structured entry path — 40 hours combined prelicensing and a single Pearson VUE appointment (code 03)

- Less competition — Fewer agents per capita than neighboring states

- Solid compensation — U.S. median annual wage for insurance sales agents was $60,370 in May 2024 (U.S. Bureau of Labor Statistics)

Start Your FREE West Virginia P&C Exam Prep

Ready to begin studying? Our comprehensive, completely free West Virginia P&C exam prep covers everything you need to pass.

Key Topics Covered on the Exam

1. Property Policies and Forms

Homeowners Insurance:

- HO-2, HO-3, HO-4, HO-5, HO-6, HO-8 policy forms

- Coverage A (Dwelling), B (Other Structures), C (Personal Property)

- Coverage D (Loss of Use), E (Personal Liability)

- Dwelling fire policies (DP-1, DP-2, DP-3)

West Virginia-Specific Property Topics:

- West Virginia FAIR Plan (residual market)

- Flood insurance (major WV exposure; NFIP participation)

- Landslide and earth movement coverage

- Mine subsidence coverage (W. Va. Code §33-30)

- Mountain terrain property considerations

Commercial Property:

- Building and personal property coverage forms

- Business income coverage

- Equipment breakdown

- Inland marine coverage

2. Casualty and Liability Policies

Personal Liability:

- Homeowners liability (Coverage E)

- Personal umbrella policies

- Medical payments coverage

Commercial Liability:

- Commercial General Liability (CGL)

- Products and completed operations

- Professional liability (E&O)

- Workers' compensation requirements

West Virginia Workers' Compensation:

- Required for most employers unless exempt

- Competitive market with licensed private carriers

- Self-insurance options for qualified employers

- Employers' liability remains Part Two of the policy

3. Auto Insurance and Commercial Casualty

West Virginia Auto Insurance Requirements:

| Coverage | Minimum Limit |

|---|---|

| Bodily Injury (per person) | $25,000 |

| Bodily Injury (per accident) | $50,000 |

| Property Damage | $25,000 |

| Uninsured Motorist (BI) | $25,000/$50,000 |

| Uninsured Motorist (PD) | $25,000 |

Underinsured motorist coverage is a mandatory optional offering — insurers must offer it, but the insured may reject it in writing. Higher UM limits up to 100/300/50 must also be offered.

Additional Auto Topics:

- Personal Auto Policy (PAP) coverage parts

- West Virginia financial responsibility law

- Uninsured motorist coverage (required)

- Underinsured motorist coverage (must be offered)

- SR-22 requirements

- Commercial auto insurance

4. West Virginia Insurance Code and Regulations

Chapter 33 Key Provisions:

- Producer licensing requirements

- Unfair trade practices

- Unfair claims settlement practices

- Policy cancellation and nonrenewal rules

- Advertising guidelines

- West Virginia Automobile Insurance Plan (Assigned Risk)

- West Virginia Property and Casualty Insurance Guaranty Association

Licensing Requirements:

- Pre-licensing education: 20 hours per line, 40 hours combined for P&C

- Pre-licensing certificate valid for 6 months from completion date

- Continuing education: 24 hours every 2 years (3 hours ethics included)

- Background check / fingerprinting required for resident applicants

- Eight-test lifetime limit per W. Va. Code §33-12-5

5. Producer Conduct and Ethics

- Fiduciary duties to insureds

- Premium handling requirements

- Claims reporting obligations

- Privacy and confidentiality

Study Timeline for Success

| Week | Focus Area | Hours |

|---|---|---|

| Week 1-2 | Property insurance fundamentals | 12-14 |

| Week 2-3 | Liability insurance | 12-14 |

| Week 3-4 | Auto insurance and WV requirements | 12-14 |

| Week 4 | West Virginia regulations (Ch. 33) | 8-10 |

| Week 5 | Practice exams and review | 12-14 |

Total recommended study time: 55-65 hours

Free Practice Questions Available

Test your knowledge with hundreds of free practice questions designed specifically for the West Virginia P&C exam.

West Virginia-Specific Exam Tips

1. Know West Virginia Auto Minimums

West Virginia requires 25/50/25 liability coverage plus 25/50/25 uninsured motorist coverage:

- $25,000 per person bodily injury

- $50,000 per accident bodily injury

- $25,000 property damage

- $25,000/$50,000 uninsured motorist (BI), plus $25,000 UM property damage

Underinsured motorist coverage is a mandatory optional offering — the insurer must offer it, but you may reject it.

2. Master Flood Coverage

West Virginia has significant flood exposure:

- River valleys — Primary flood risk areas

- Flash flooding — Mountain terrain accelerates runoff

- NFIP participation — National Flood Insurance Program

- Flood exclusions — Standard policies exclude flood

- Flood training — Resident producers selling federal flood policies must complete a one-time 3-hour NFIP course

3. Understand Mining-Related Coverage

West Virginia's mining heritage creates unique exposures:

- Mine subsidence coverage (W. Va. Code §33-30)

- Earth movement considerations

- Environmental liability

- Equipment and machinery coverage

4. Key Numbers to Remember

| Topic | West Virginia Requirement |

|---|---|

| Auto minimums | 25/50/25 liability + 25/50/25 UM |

| WC threshold | Most employers |

| Pre-licensing | 40 hours combined (20 per line) |

| Pre-licensing validity | 6 months from completion |

| CE requirement | 24 hours/2 years (3 ethics) |

| License renewal | Biennial, last day of birth month |

| Passing score | 70 scaled score |

| Exam attempts | 8 per lifetime (W. Va. Code §33-12-5) |

Common Mistakes to Avoid

- Underestimating flood exposure — Major WV property concern

- Not knowing auto minimums — WV is 25/50/25 plus required UM at the same limits

- Ignoring mine subsidence — Important for many WV properties

- Forgetting UM coverage — Required in West Virginia, not optional

- Not practicing timed exams — 210 minutes for 158 questions on the combined exam

- Cramming last minute — Spread study over 4-5 weeks

- Treating state law as a side topic — West Virginia laws and rules are 29% of the combined exam (40 of 140 scored questions)

After Passing Your Exam

- Get fingerprinted — Schedule at an IdentoGo facility after passing; results go to the WV OIC. The fingerprint receipt includes a 12-digit TCN you enter on your license application.

- Apply for license — Submit the resident producer application through NIPR and pay the $50 license fee.

- Affiliate with insurer — Get appointed by a carrier (carrier files appointment with OIC).

- Maintain CE compliance — 24 hours every 2 years, including 3 hours of ethics, before renewal.

- Renew on time — License expires the last day of your birth month every two years; renew through NIPR.

If you fail the exam, you may reschedule immediately but must wait 24 hours before booking. Repeated failures matter: West Virginia caps lifetime exam attempts at eight per W. Va. Code §33-12-5.

2026 West Virginia Updates

As of July 2026, the current Pearson VUE / OIC licensing path reflects:

- Pearson VUE as the testing vendor (candidate handbook stock 1249-01)

- Combined P&C exam (code 03): 140 scored questions plus 18 pretest (158 total) in 210 minutes

- Separate Property (code 30) and Casualty (code 40) exams also available, each 80 scored questions in 120 minutes

- 40 hours of combined prelicensing (20 per line), certificate valid 6 months

- $84 exam fee per appointment

- $45.75 fingerprinting fee through IdentoGo (vendor-set, confirm current amount)

- $50 resident license application fee through NIPR

Start Your West Virginia P&C Insurance Career Today

The West Virginia P&C license opens doors to a specialized regional insurance market. With proper preparation, you can pass the exam on your first attempt.

Our free study materials include:

- Complete topic coverage

- Practice questions with explanations

- West Virginia-specific regulations (Chapter 33)

- Study guides and summaries

- AI-powered study assistance

Don't pay for expensive prep courses when everything you need is available FREE.

How to Verify the Rules Before You Schedule

Use this guide for exam strategy, then confirm the current licensing steps with official sources before you pay for an appointment. Property and casualty licensing is state-administered, and administrative details can change even when the insurance concepts stay the same. Check the West Virginia insurance department first, then the testing vendor candidate handbook, then the application path used after passing. The NAIC state insurance department directory is the safest way to find the current regulator site, and NIPR state requirements can help you confirm post-exam application steps.

For exam content, keep two buckets separate. The national bucket includes property policies, casualty policies, liability principles, negligence, risk management, policy structure, exclusions, conditions, endorsements, and claims concepts. The West Virginia bucket includes regulator authority, producer licensing, unfair practices, cancellation and nonrenewal rules, state auto requirements, residual market mechanisms, and local compliance duties. When a question includes a deadline, dollar limit, filing duty, required notice, or licensing step, ask whether it is a general insurance concept or a West Virginia rule.

What to Master for Property Questions

Property questions reward careful reading. Know the difference between named-peril and open-peril coverage, replacement cost and actual cash value, direct and indirect loss, vacancy and unoccupancy, and first-party property coverage versus third-party liability. Homeowners forms are a frequent source of points because the forms look similar but solve different problems. Practice identifying who is insured, what property is covered, which location qualifies as the residence premises, and whether the loss is excluded before an endorsement changes the answer.

Do not treat deductibles, limits, and valuation as afterthoughts. A question may describe a covered loss but test whether the settlement is reduced by deductible, limited by a sublimit, valued at actual cash value, or excluded because the cause of loss is not covered. Commercial property questions add business personal property, business income, extra expense, equipment breakdown, inland marine, and builder's risk concepts. For commercial forms, focus on why a business would need the coverage and what exposure remains if it does not have it.

What to Master for Casualty and Liability Questions

Casualty questions often turn on liability logic. Before choosing an answer, identify the claimant, the insured, the alleged injury or damage, and the legal theory. Negligence questions usually require duty, breach, causation, and damages. Liability policy questions ask whether the policy responds to bodily injury, property damage, personal and advertising injury, medical payments, or a specifically excluded exposure.

For auto, separate personal auto policy structure from state financial responsibility requirements. You need to know liability, medical payments or personal injury protection where relevant, uninsured and underinsured motorist concepts, damage to your auto, covered auto definitions, exclusions, and endorsements. For commercial auto, pay attention to covered auto symbols, hired and non-owned autos, business use, and garage exposures. For workers' compensation, separate statutory benefits from employer liability and remember that workers' compensation is not ordinary negligence coverage.

Final Two-Week Study Plan

In the first week, rotate by coverage family: homeowners and dwelling property, commercial property, personal auto, commercial auto, general liability, workers' compensation, and West Virginia law. After every practice set in /study-guides/wv-property-casualty, write down whether each miss was caused by vocabulary, form structure, state rule, or careless reading. Vocabulary misses need flashcards. Form structure misses need diagrams. State-rule misses need a one-page West Virginia checklist. Careless reading needs slower question markup.

In the second week, stop studying by chapter only. The actual exam mixes topics, so your practice should mix them too. Use timed sets and force yourself to decide quickly whether the question is asking about coverage trigger, excluded cause, valuation, limit, condition, producer conduct, or state filing rule. Review explanations immediately. The review is where your score improves; simply taking more questions without fixing the reason for misses mostly measures the same weakness again.

Common P&C Exam Traps

One trap is choosing the coverage that sounds familiar instead of the coverage that fits the loss. A flood loss, an employee injury, a professional advice claim, a business income interruption, and a personal auto collision may all involve money damages, but they do not belong in the same policy part. Another trap is ignoring who owns the property or who is legally liable. Property insurance usually protects the insured's financial interest in property; liability insurance responds to claims made by others against the insured.

Cancellation and nonrenewal questions also deserve attention. The exam may test required notice, permitted reasons, timing, or who has authority to act. If the question is state-specific, do not rely on a generic national rule. Unfair trade practice questions work the same way: rebating, twisting, misrepresentation, false advertising, unfair claims handling, and fiduciary misuse of premiums are tested because they show whether a producer can operate lawfully after the exam.

Exam-Day Workflow

Confirm your appointment, identification, remote-proctoring rules, allowed materials, and reschedule deadline before test day. At check-in, your legal name should match the exam registration. During the test, take the easy points first. If a scenario is long, identify the policy, the insured, the covered property or claimant, the cause of loss, and the question's command word. If two answers are legally true, choose the one that answers the exact fact pattern.

If you miss the passing score, use the report as a map. Rebuild the two weakest content areas, then retest with mixed questions. Candidates often improve fastest by mastering policy architecture: declarations, insuring agreement, conditions, exclusions, definitions, and endorsements. Once you can locate where a rule lives inside the policy, unfamiliar questions become easier to reason through.