Colorado Property & Casualty Insurance License Exam Overview

Colorado licenses Property and Casualty as two separate lines of authority, each with its own exam — there is no single combined "P&C" test. Both exams are administered by Pearson VUE on behalf of the Colorado Division of Insurance (DOI), part of the Department of Regulatory Agencies (DORA). Colorado switched its insurance licensing vendor to Pearson VUE; Prometric no longer administers this exam.

Most candidates want both authorities, so Pearson VUE lets you schedule Property and Casualty back-to-back in one test-center visit. Passing both qualifies you to sell property insurance, auto insurance, liability coverage, and related products throughout Colorado — a state that crossed 6 million residents in 2025, with the Front Range generating more hail claims than almost anywhere else in the country and a fast-growing wildfire-exposed mountain corridor.

Exam Format at a Glance

| Component | Property Exam | Casualty Exam |

|---|---|---|

| Scored Questions | 75 (50 general + 25 Colorado-specific) | 81 (50 general + 31 Colorado-specific) |

| Unscored Pretest Questions | 10 (not counted toward your score) | 10 (not counted toward your score) |

| Time Limit | 2 hours | 2 hours |

| Passing Score | Scaled score equal to 70% mastery | Scaled score equal to 70% mastery |

| Testing Vendor | Pearson VUE | Pearson VUE |

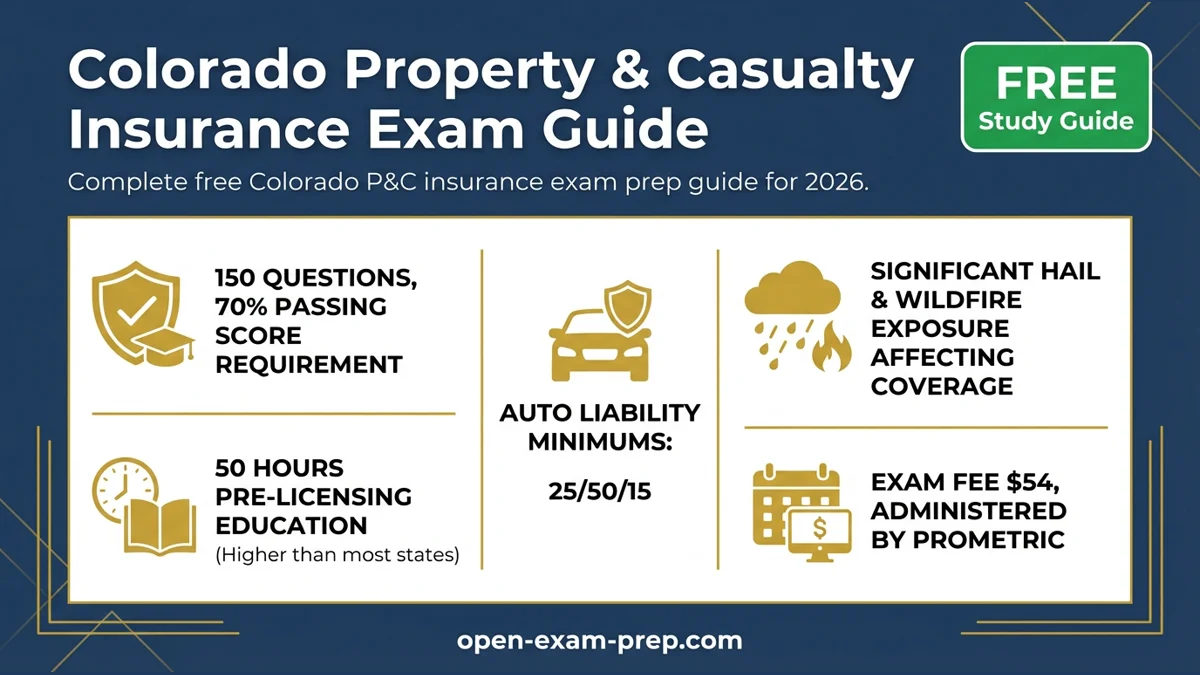

Exam fee: at a physical Pearson VUE test center, you can take up to two exams in one session for a single $41 fee — so scheduling Property and Casualty together costs $41 total, not $41 each. Each exam taken alone through Pearson VUE's online OnVUE platform costs $31. Both exams are graded independently — passing Property and failing Casualty (or vice versa) means you only need to retest the one you failed.

Pre-licensing education: Colorado requires 50 hours of approved pre-licensing study before each major line exam — for example, 50 hours before the Property exam and 50 hours before the Casualty exam (training providers can waive duplicate "Principles of Insurance" hours if you complete both lines through the same course). This is meaningfully more than the 20–40 hours many states require and is one of the reasons Colorado-licensed producers tend to walk in better prepared.

Why Get P&C Licensed in Colorado?

- Large, growing market — Colorado passed 6 million residents in 2025, and the Denver metro continues to add corporate relocations and new households that all need property and auto coverage

- High hail exposure — the Front Range (Denver, Colorado Springs, Boulder) generates some of the highest hail-claim volumes in the nation, creating steady demand for knowledgeable property producers

- Growing wildfire market — Colorado launched a state-backed FAIR Plan insurer of last resort in April 2025 for wildfire-exposed homes private carriers won't write, opening a new niche for producers who understand it

- Higher entry bar, less competition — the 50-hour pre-licensing requirement screens out under-prepared applicants compared to lighter-touch states

📚 Start Your FREE Colorado P&C Exam Prep

Ready to begin studying? Our comprehensive, completely free Colorado P&C exam prep covers everything you need to pass both exams.

What's Actually Tested: The Official Pearson VUE Content Outlines

Colorado publishes separate content outlines for each exam. Knowing the exact point allocation tells you where to spend study time.

Property Exam (75 scored questions)

General Knowledge section (50 questions):

- Types of policies (22 pts) — Homeowners HO-2/HO-3/HO-4/HO-5/HO-6/HO-8, Dwelling DP-1/DP-2/DP-3, Commercial Package Policy, Business Owners Policy, Builders Risk, Cyber first-party coverage, inland marine (personal articles and commercial property floaters), the National Flood Insurance Program, earthquake, mobile homes, watercraft, farmowners, and windstorm

- Insurance terms and related concepts (15 pts) — law of large numbers, insurable interest, peril vs. hazard (moral/morale/physical), direct vs. indirect loss, actual cash value vs. replacement cost vs. market/stated/agreed value, proximate cause, coinsurance, vacancy and unoccupancy

- Policy provisions and contract law (13 pts) — declarations, insuring agreement, conditions, exclusions, who is insured, duties after loss, mortgagee rights, subrogation

Colorado-Specific section (25 questions):

- Statutes common to Life, Sickness & Accident, Property, and Casualty (19 pts) — Insurance Commissioner powers, licensing, unfair trade practices, rebating, fraud statute

- Statutes common to Property and Casualty only (4 pts) — rate regulation, summary disclosure form, commercial policy requirements, use of credit information

- Statutes pertinent to Property only (2 pts) — fraudulent claims/arson reporting, homeowners cancellation and nonrenewal, availability of fire insurance

Casualty Exam (81 scored questions)

General Knowledge section (50 questions):

- Types of policies, bonds, and related terms (23 pts) — Commercial General Liability (premises/operations, products/completed operations, Coverage A/B/C, per-occurrence and aggregate limits), personal and business auto liability, workers' compensation and employers liability, crime (employee dishonesty, theft, burglary), surety and fidelity bonds, professional liability (E&O, D&O, EPLI, cyber, liquor liability), umbrella/excess liability

- Insurance terms and related concepts (15 pts) — risk, hazards, indemnity, insurable interest, loss valuation, negligence, liability theories, binders, warranties, concealment

- Policy provisions (12 pts) — declarations, conditions, exclusions, duties after a loss, cancellation/nonrenewal, subrogation, Terrorism Risk Insurance Act (TRIA)

Colorado-Specific section (31 questions):

- Statutes common to Life, Sickness & Accident, Property, and Casualty (19 pts) — same regulator/licensing/unfair-practices block as the Property exam

- Statutes common to Property and Casualty only (4 pts) — rate regulation, summary disclosure form, commercial policy requirements

- Statutes pertinent to Casualty only (8 pts) — workers' compensation coverage requirements, auto cancellation/nonrenewal, excluded drivers, and uninsured/underinsured motorist rules

Colorado Auto Insurance Requirements (tested on the Casualty exam)

| Coverage | Minimum Limit |

|---|---|

| Bodily Injury (per person) | $25,000 |

| Bodily Injury (per accident) | $50,000 |

| Property Damage | $15,000 |

Colorado is an at-fault (tort) state with a modified comparative negligence rule: an injured driver who is found more than 50% at fault cannot recover damages. The Casualty exam also tests Personal Auto Policy structure, uninsured/underinsured motorist coverage (insurers must offer it; drivers can reject it in writing), SR-22 financial responsibility filings, and commercial auto exposures like hired and non-owned autos.

Colorado Workers' Compensation (tested on the Casualty exam)

- Nearly universal requirement — Colorado requires workers' compensation coverage for virtually every employer with at least one employee, full- or part-time, including family members; narrow exemptions exist for certain casual/domestic workers and most sole proprietors outside construction

- Pinnacol Assurance remains Colorado's largest workers' comp carrier, covering more than 50,000 businesses, but Colorado is a competitive state — employers may buy coverage from any licensed carrier, not just Pinnacol

- The exam tests statutory benefits, exclusive remedy, employer's liability, and the difference between workers' comp and ordinary negligence coverage

Colorado-Specific Property Risk Topics

- Colorado FAIR Plan — launched April 2025 as the state's insurer of last resort for residential properties (commercial properties followed shortly after) that private carriers decline because of wildfire risk; expect questions on when a property qualifies and what the plan does and doesn't cover

- House Bill 25-1182 (effective July 1, 2026) requires insurers to disclose how they model wildfire risk and how mitigation steps can lower premiums — a new 2026 compliance topic worth knowing even if it isn't yet on the published content outline

- Hail damage — the leading property claim type on the Front Range; know percentage deductibles (common for roof/hail claims), replacement cost vs. actual cash value settlement, and cosmetic-damage exclusion endorsements

- Wildfire and mountain-community exposure — defensible space/mitigation requirements, evacuation-related coverage questions, and how mitigation work can affect eligibility and premium

Licensing Requirements Beyond the Exam

- Pre-licensing education: 50 hours per major line (Property and Casualty each), completed through an approved provider before you can sit for that exam

- Continuing education: 24 hours every 2-year license continuation cycle, including 3 hours of ethics; first-time licensees are exempt from CE until their second continuation cycle

- Background check and fingerprinting: required for all resident producer applicants through the state's approved vendor

- Application: submitted online through Sircon or NIPR, not a generic "DOI portal" — Pearson VUE reports your passing score directly to the Division

Study Timeline for Success

| Week | Focus Area | Hours |

|---|---|---|

| Week 1-2 | Property general-knowledge content (homeowners forms, commercial property, valuation) | 14-16 |

| Week 2-3 | Casualty general-knowledge content (CGL, auto, workers' comp, bonds) | 14-16 |

| Week 3-4 | Colorado-specific statutes shared by both exams (Title 10 C.R.S.) | 10-12 |

| Week 4-5 | Property-only and Casualty-only Colorado statutes, auto minimums, WC rules | 10-12 |

| Week 5-6 | Timed practice exams and review for both exams | 12-14 |

Total recommended study time: 60-80 hours across both exams (on top of the required 50 hours of pre-licensing coursework per line).

🎯 Free Practice Questions Available

Test your knowledge with hundreds of free practice questions covering both the Property and Casualty content outlines, with Colorado-specific scenarios built in.

Common Mistakes to Avoid

- Assuming it's one combined exam — it's two separate exams with separate scores; study and schedule accordingly

- Underestimating pre-licensing — Colorado requires 50 hours per line (much higher than many states)

- Skipping hail coverage — the primary Colorado property risk and a frequent Property-exam topic

- Ignoring the new FAIR Plan and HB 25-1182 — current Colorado-specific material competitors and older guides miss

- Not knowing auto minimums — Colorado is 25/50/15, tested on the Casualty exam

- Not practicing timed, mixed-topic sets — each exam gives you 2 hours; don't run out of time on the general-knowledge half

- Cramming last minute — spread study over 5-6 weeks per exam

After Passing Your Exams

- Apply for your license online at Sircon or NIPR — Pearson VUE transmits your scores directly, so there's no separate score-reporting step

- Complete fingerprinting through the state's approved vendor if you haven't already

- Pay the license application fee — $44 per line of authority for a new resident license, so $88 total if you're applying for both Property and Casualty at once

- Affiliate with an insurer — get appointed by the carrier(s) you'll represent

- Maintain CE compliance — 24 hours every 2-year continuation cycle, including 3 ethics hours, starting with your second cycle

- Begin selling — your producer license is perpetual as long as you pay the continuation fee and meet CE requirements on time (Colorado has no grace period for continuation)

Start Your Colorado P&C Insurance Career Today

The Colorado P&C license opens doors to one of the nation's fastest-growing insurance markets. With proper preparation, you can pass both exams on your first attempt.

Our free study materials include:

- ✅ Complete coverage of both Property and Casualty content outlines

- ✅ Practice questions with explanations

- ✅ Colorado-specific regulations (Title 10 C.R.S.), the FAIR Plan, and HB 25-1182

- ✅ Study guides and summaries

- ✅ AI-powered study assistance

Don't pay for expensive prep courses when everything you need is available FREE.

How to Verify the Rules Before You Schedule

Use this guide for exam strategy, then confirm the current licensing steps with official sources before you pay for an appointment. Property and casualty licensing is state-administered, and administrative details — fees, vendors, hour requirements — can change even when the underlying insurance concepts stay the same. Check the Colorado Division of Insurance first, then the Pearson VUE Colorado candidate handbook, then the application path used after passing (Sircon or NIPR). The NAIC state insurance department directory is the safest way to find the current regulator site if a link goes stale.

For exam content, keep two buckets separate. The national/general-knowledge bucket includes property policies, casualty policies, liability principles, negligence, risk management, policy structure, exclusions, conditions, endorsements, and claims concepts — identical in spirit to what other states test. The Colorado bucket includes regulator authority, producer licensing, unfair practices, cancellation and nonrenewal rules, state auto requirements, the FAIR Plan residual market, and local compliance duties. When a question includes a deadline, dollar limit, filing duty, required notice, or licensing step, ask whether it is a general insurance concept or a Colorado-specific rule.

What to Master for Property Questions

Property questions reward careful reading. Know the difference between named-peril and open-peril coverage, replacement cost and actual cash value, direct and indirect loss, vacancy and unoccupancy, and first-party property coverage versus third-party liability. Homeowners forms are a frequent source of points because the forms look similar but solve different problems. Practice identifying who is insured, what property is covered, which location qualifies as the residence premises, and whether the loss is excluded before an endorsement changes the answer.

Do not treat deductibles, limits, and valuation as afterthoughts. A question may describe a covered loss but test whether the settlement is reduced by deductible, limited by a sublimit, valued at actual cash value, or excluded because the cause of loss is not covered. Commercial property questions add business personal property, business income, extra expense, equipment breakdown, inland marine, and builder's risk concepts. For commercial forms, focus on why a business would need the coverage and what exposure remains if it does not have it.

What to Master for Casualty and Liability Questions

Casualty questions often turn on liability logic. Before choosing an answer, identify the claimant, the insured, the alleged injury or damage, and the legal theory. Negligence questions usually require duty, breach, causation, and damages. Liability policy questions ask whether the policy responds to bodily injury, property damage, personal and advertising injury, medical payments, or a specifically excluded exposure.

For auto, separate personal auto policy structure from Colorado's financial responsibility requirements. You need to know liability, medical payments, uninsured and underinsured motorist concepts, damage to your auto, covered auto definitions, exclusions, and endorsements. For commercial auto, pay attention to covered auto symbols, hired and non-owned autos, business use, and garage exposures. For workers' compensation, separate statutory benefits from employer liability and remember that workers' compensation is not ordinary negligence coverage.

Final Two-Week Study Plan

In the second week, stop studying by chapter only. Each actual exam mixes topics across its general-knowledge and Colorado sections, so your practice should mix them too. Use timed sets and force yourself to decide quickly whether the question is asking about coverage trigger, excluded cause, valuation, limit, condition, producer conduct, or state filing rule. Review explanations immediately. The review is where your score improves; simply taking more questions without fixing the reason for misses mostly measures the same weakness again.

Common P&C Exam Traps

One trap is choosing the coverage that sounds familiar instead of the coverage that fits the loss. A flood loss, an employee injury, a professional advice claim, a business income interruption, and a personal auto collision may all involve money damages, but they do not belong in the same policy or the same exam. Another trap is ignoring who owns the property or who is legally liable. Property insurance usually protects the insured's financial interest in property; liability insurance responds to claims made by others against the insured.

Cancellation and nonrenewal questions also deserve attention. The exam may test required notice, permitted reasons, timing, or who has authority to act. If the question is Colorado-specific, do not rely on a generic national rule. Unfair trade practice questions work the same way: rebating, twisting, misrepresentation, false advertising, unfair claims handling, and fiduciary misuse of premiums are tested because they show whether a producer can operate lawfully after the exam.

Exam-Day Workflow

Confirm your appointment(s), identification, OnVUE remote-proctoring rules (if testing online), allowed materials, and reschedule deadline before test day — you must cancel or change at least 48 hours ahead or you forfeit the fee. At check-in, bring two forms of signature ID (one government-issued photo ID); your legal name must match your registration. During each exam, take the easy points first. If a scenario is long, identify the policy, the insured, the covered property or claimant, the cause of loss, and the question's command word. If two answers are legally true, choose the one that answers the exact fact pattern.

If you miss the passing score on either exam, use the score report as a map — Colorado reports a scaled score (0-100) to failing candidates so you can see how close you came, though not the exact number of questions missed. Rebuild your two weakest content areas, then retest with mixed questions after the required 24-hour waiting period. Candidates often improve fastest by mastering policy architecture: declarations, insuring agreement, conditions, exclusions, definitions, and endorsements. Once you can locate where a rule lives inside the policy, unfamiliar questions become easier to reason through.