California Property & Casualty Insurance License Exam Overview

The California Property and Casualty Broker-Agent license exam is administered by PSI Services on behalf of the California Department of Insurance (CDI). California is the largest insurance market in the nation, with unique challenges including wildfires, earthquakes, and the strictest rate regulation in the country under Proposition 103.

Passing this exam qualifies you to transact property, casualty, and auto insurance in California, serving nearly 40 million residents with unmatched demand for homeowners, auto, and commercial coverage. The combined Property and Casualty exam covers both the property line and the casualty (liability) line in a single sitting; CDI also offers stand-alone Property Broker-Agent and Casualty Broker-Agent exams (75 questions each, 1.5 hours each) if you only need one line.

2026 alert (AB 943): Effective January 1, 2026, California removed the 20-hour line-specific prelicensing requirement for property, casualty, personal lines, and most other producer licenses. The only mandatory prelicensing course now is the 12-hour Code and Ethics course - down from the old 52-hour total. The exam itself did not change, so with less required coursework, self-study quality matters more than ever.

Exam Format at a Glance

| Component | Details |

|---|---|

| License | Property and Casualty Broker-Agent (combined) |

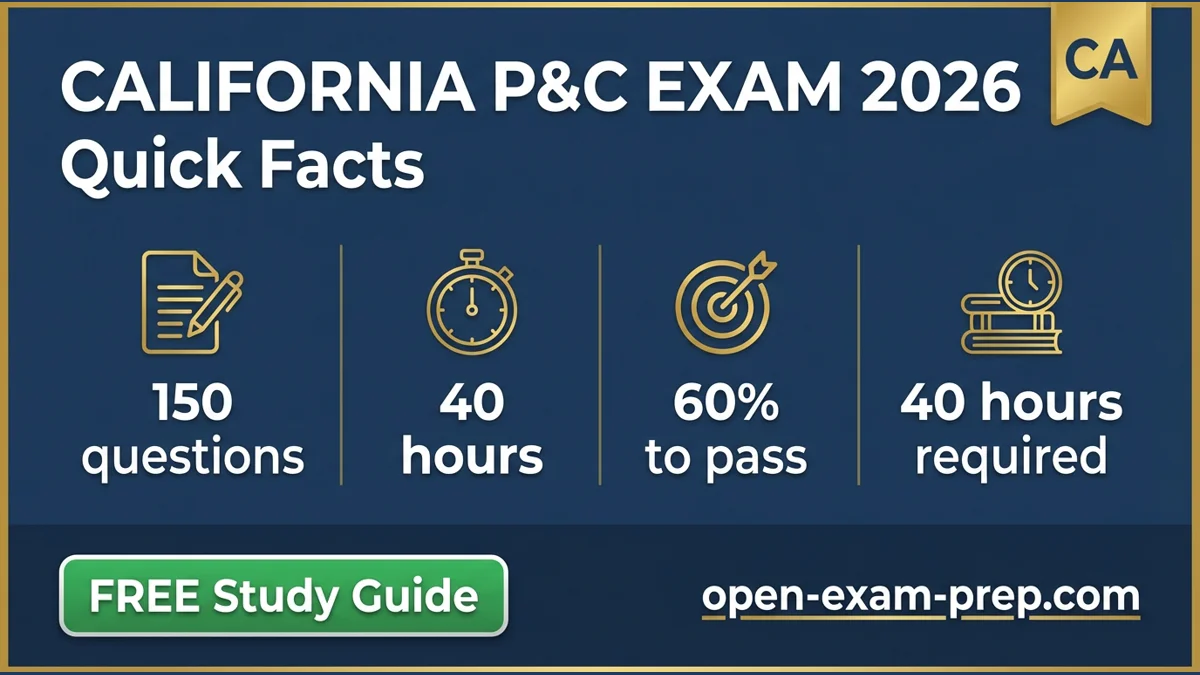

| Total Questions | 150 multiple-choice (scored) |

| Time Limit | 3 hours (180 minutes) |

| Passing Score | 60% (90 of 150 correct) |

| Exam Fee | $88 base + $33 PSI convenience fee (about $121) |

| Prelicensing Education | 12-hour Code and Ethics course required (AB 943, eff. 1/1/2026) |

| Testing Vendor | PSI Services for CDI |

| Delivery | In-person test center or online remote proctoring |

| License Term | 2 years |

Note on the 60% pass mark: California is unusual. Every CDI producer license exam passes at 60%, well below the 70% common in many other states. A lower threshold does not make the exam easy - the questions are detailed, scenario-based, and heavy on California-specific law.

Why Get P&C Licensed in California?

- Largest state market - Nearly 40 million residents

- High property values - Significant premium volume

- Wildfire coverage needs - Specialty market growing

- Auto insurance required - Every driver needs coverage

- Commercial opportunities - Business insurance demand

📚 Start Your FREE California P&C Exam Prep

Ready to begin studying? Our comprehensive, completely free California P&C exam prep covers everything you need to pass.

Key Topics Covered on the Exam

1. Property Insurance (30%)

Homeowners Insurance:

- HO-2, HO-3, HO-4, HO-5, HO-6, HO-8 forms

- Coverage A through F breakdown

- California-specific endorsements

- Replacement cost vs. actual cash value

California FAIR Plan:

- Fair Access to Insurance Requirements

- Insurer of last resort for fire coverage

- Wildfire-prone area coverage

- Eligibility requirements

- Coverage limits and limitations

California Earthquake Authority (CEA):

- Mini-policy structure

- Deductible options (5%, 10%, 15%, 25%)

- Coverage limitations

- What's covered vs. excluded

- Separate from homeowners policy

Commercial Property:

- Building and personal property coverage

- Business interruption insurance

- Builder's risk coverage

- Inland marine

2. Casualty/Liability Insurance (30%)

Personal Liability:

- Homeowners liability coverage (Coverage E)

- Personal umbrella policies

- Medical payments coverage

Commercial Liability:

- Commercial General Liability (CGL)

- Professional liability (E&O)

- Products and completed operations

- Employment practices liability

Workers' Compensation:

- California mandatory coverage

- State Compensation Insurance Fund (SCIF)

- Employer penalties for non-compliance

- Premium calculation

- Experience modification

3. Auto Insurance (20%)

California Financial Responsibility Law (UPDATED - 30/60/15 since Jan 1, 2025):

Senate Bill 1107 (the Protect California Drivers Act) raised California's minimum auto liability limits for the first time since 1967. As of January 1, 2025 the minimums are 30/60/15 - old study materials and any "15/30/5" answer choice are now WRONG.

| Coverage | Minimum (current) | Old (pre-2025) |

|---|---|---|

| Bodily Injury (per person) | $30,000 | $15,000 |

| Bodily Injury (per accident) | $60,000 | $30,000 |

| Property Damage (per accident) | $15,000 | $5,000 |

Under SB 1107 these limits hold until 2035, when they rise again to 50/100/25. Expect the exam to test the current 30/60/15 figures.

Additional Auto Topics:

- California Low Cost Automobile (CLCA) Insurance Program for income-eligible drivers

- Good Driver Discount (at least 20% below the otherwise-applicable rate; mandatory)

- Uninsured and underinsured motorist coverage (offer/waiver rules)

- California Automobile Assigned Risk Plan (CAARP) residual market

- Proposition 103 prior-approval rate regulation

4. California Insurance Code (15%)

Key Regulations:

- Proposition 103 (voter-approved rate regulation)

- Prior approval requirements for rates

- Rate rollback provisions

- Good driver discount mandate

CDI Authority:

- California Department of Insurance powers

- Consumer complaint process

- Market conduct examinations

- Enforcement actions

Prohibited Practices:

- Rebating and inducements

- Misrepresentation

- Twisting and churning

- Unfair discrimination

- Unfair claims settlement practices

5. Ethics and General Insurance (5%)

Producer Responsibilities:

- Fiduciary duties

- Premium trust requirements

- Client disclosure obligations

- Surplus lines placement

Continuing Education:

- 24 hours every 2 years (Property and/or Casualty Broker-Agent)

- Must include 3 hours of approved ethics CE each renewal period

- CDI-approved courses only

Study Timeline for Success

| Week | Focus Area | Hours |

|---|---|---|

| Week 1-2 | Property insurance, FAIR Plan, CEA | 14-16 |

| Week 2-3 | Liability insurance and workers' comp | 12-15 |

| Week 3-4 | Auto insurance and CA minimums | 10-12 |

| Week 4-5 | California Insurance Code, Prop 103 | 10-12 |

| Week 5-6 | Practice exams and review | 12-15 |

Total recommended study time: 58-70 hours. Since AB 943 no longer mandates the 20-hour line-specific course, this self-study block is now the core of your preparation (only the 12-hour Code and Ethics course is still required).

🎯 Free Practice Questions Available

Test your knowledge with free, exam-style practice questions built specifically for the California P&C exam, with full explanations.

California-Specific Exam Tips

1. Master the FAIR Plan

California's FAIR Plan is essential:

- Insurer of last resort for fire coverage

- Critical for wildfire-prone areas

- Know eligibility requirements

- Understand coverage limitations vs. standard policies

2. Understand California Earthquake Authority (CEA)

Earthquake coverage is unique to California:

- Not included in standard homeowners

- Mini-policy with limited coverage

- High deductibles (5-25%)

- Know what's covered and excluded

3. Know Proposition 103

California's unique rate regulation:

- Prior approval required for rate changes

- Good driver discount mandatory (20%)

- Rate rollback provisions

- Consumer Watchdog oversight

4. Key Numbers to Remember

| Topic | California Requirement |

|---|---|

| Passing score | 60% (90/150) |

| Exam questions / time | 150 questions / 3 hours |

| Prelicensing (AB 943, 2026) | 12-hour Code and Ethics course |

| License term | 2 years |

| CE requirement | 24 hours/2 years (incl. 3 hrs ethics) |

| Auto BI minimums | 30/60 (was 15/30) |

| Auto PD minimum | $15,000 (was $5,000) |

| Good driver discount | 20% mandatory |

Common Mistakes to Avoid

- Ignoring FAIR Plan details - Major exam topic

- Forgetting CEA structure - Unique to California

- Missing Proposition 103 - Heavily tested

- Studying outdated 15/30/5 auto limits - California raised them to 30/60/15 on Jan 1, 2025; learn the new numbers

- Skipping workers' comp - Mandatory in California

- Not practicing enough - 150 questions needs preparation

Step-by-Step: From Prelicensing to Active License

- Complete the 12-hour Code and Ethics prelicensing course from a CDI-approved provider (the only mandatory course as of 2026 under AB 943).

- Register and schedule your exam with PSI for CDI ($88 exam fee plus a $33 PSI convenience fee, about $121).

- Pass the 150-question exam at 60% (90 correct).

- Get fingerprinted (Live Scan) through Accurate Biometrics (about $59) or a PSI test center (about $69). Fingerprints are required before a license can be issued.

- Submit your license application to CDI and pay the license fee (about $188 for the two-year term).

- Obtain a carrier appointment so you can transact on an insurer's behalf.

- Maintain CE - 24 hours every 2 years, including 3 ethics hours.

Realistic total cost: roughly $120 exam + $59 fingerprint + $188 license + the cost of the 12-hour ethics course, typically $500-$650 all-in, depending on your course provider.

2026 California Updates

Two recent law changes are the most testable, most-missed items on the current exam:

- AB 943 (eff. Jan 1, 2026): Removed the 20-hour line-specific prelicensing requirement for property, casualty, personal lines, commercial lines, limited-line auto, life, and accident/health. Only the 12-hour Code and Ethics course remains mandatory. (Bail agents and public adjusters still need full prelicensing.)

- SB 1107 (eff. Jan 1, 2025): Raised minimum auto liability limits to 30/60/15. The old 15/30/5 is obsolete.

Also stay current on:

- Wildfire insurance market and FAIR Plan capacity changes

- The Sustainable Insurance Strategy and catastrophe-modeling rules affecting rate filings

- Proposition 103 prior-approval developments

- Climate-risk disclosure requirements

Start Your California P&C Career Today

The California Property & Casualty license opens doors to serving the nation's largest insurance market with unique challenges and opportunities. With proper preparation, you can pass the exam on your first attempt.

Our free study materials include:

- ✅ Complete topic coverage

- ✅ Practice questions with explanations

- ✅ FAIR Plan and CEA specifics

- ✅ Proposition 103 coverage

- ✅ AI-powered study assistance

Don't pay for expensive prep courses when everything you need is available FREE.

How to Verify the Rules Before You Schedule

Use this guide for exam strategy, then confirm the current licensing steps with official sources before you pay for an appointment. Property and casualty licensing is state-administered, and administrative details can change even when the insurance concepts stay the same. Check the California insurance department first, then the testing vendor candidate handbook, then the application path used after passing. The NAIC state insurance department directory is the safest way to find the current regulator site, and NIPR state requirements can help you confirm post-exam application steps where NIPR is used.

For exam content, keep two buckets separate. The national bucket includes property policies, casualty policies, liability principles, negligence, risk management, policy structure, exclusions, conditions, endorsements, and claims concepts. The California bucket includes regulator authority, producer licensing, unfair practices, cancellation and nonrenewal rules, state auto requirements, residual market mechanisms, and local compliance duties. When a question includes a deadline, dollar limit, filing duty, required notice, or licensing step, ask whether it is a general insurance concept or a California rule.

What to Master for Property Questions

Property questions reward careful reading. Know the difference between named-peril and open-peril coverage, replacement cost and actual cash value, direct and indirect loss, vacancy and unoccupancy, and first-party property coverage versus third-party liability. Homeowners forms are a frequent source of points because the forms look similar but solve different problems. Practice identifying who is insured, what property is covered, which location qualifies as the residence premises, and whether the loss is excluded before an endorsement changes the answer.

Do not treat deductibles, limits, and valuation as afterthoughts. A question may describe a covered loss but test whether the settlement is reduced by deductible, limited by a sublimit, valued at actual cash value, or excluded because the cause of loss is not covered. Commercial property questions add business personal property, business income, extra expense, equipment breakdown, inland marine, and builder's risk concepts. For commercial forms, focus on why a business would need the coverage and what exposure remains if it does not have it.

What to Master for Casualty and Liability Questions

Casualty questions often turn on liability logic. Before choosing an answer, identify the claimant, the insured, the alleged injury or damage, and the legal theory. Negligence questions usually require duty, breach, causation, and damages. Liability policy questions ask whether the policy responds to bodily injury, property damage, personal and advertising injury, medical payments, or a specifically excluded exposure.

For auto, separate personal auto policy structure from state financial responsibility requirements. You need to know liability, medical payments or personal injury protection where relevant, uninsured and underinsured motorist concepts, damage to your auto, covered auto definitions, exclusions, and endorsements. For commercial auto, pay attention to covered auto symbols, hired and non-owned autos, business use, and garage exposures. For workers' compensation, separate statutory benefits from employer liability and remember that workers' compensation is not ordinary negligence coverage.

Final Two-Week Study Plan

In the first week, rotate by coverage family: homeowners and dwelling property, commercial property, personal auto, commercial auto, general liability, workers' compensation, and California law. After every practice set in /practice/ca-property-casualty, write down whether each miss was caused by vocabulary, form structure, state rule, or careless reading. Vocabulary misses need flashcards. Form structure misses need diagrams. State-rule misses need a one-page California checklist. Careless reading needs slower question markup.

In the second week, stop studying by chapter only. The actual exam mixes topics, so your practice should mix them too. Use timed sets and force yourself to decide quickly whether the question is asking about coverage trigger, excluded cause, valuation, limit, condition, producer conduct, or state filing rule. Review explanations immediately. The review is where your score improves; simply taking more questions without fixing the reason for misses mostly measures the same weakness again.

Common P&C Exam Traps

One trap is choosing the coverage that sounds familiar instead of the coverage that fits the loss. A flood loss, an employee injury, a professional advice claim, a business income interruption, and a personal auto collision may all involve money damages, but they do not belong in the same policy part. Another trap is ignoring who owns the property or who is legally liable. Property insurance usually protects the insured's financial interest in property; liability insurance responds to claims made by others against the insured.

Cancellation and nonrenewal questions also deserve attention. The exam may test required notice, permitted reasons, timing, or who has authority to act. If the question is state-specific, do not rely on a generic national rule. Unfair trade practice questions work the same way: rebating, twisting, misrepresentation, false advertising, unfair claims handling, and fiduciary misuse of premiums are tested because they show whether a producer can operate lawfully after the exam.

Exam-Day Workflow

Confirm your appointment, identification, remote-proctoring rules, allowed materials, and reschedule deadline before test day. At check-in, your legal name should match the exam registration. During the test, take the easy points first. If a scenario is long, identify the policy, the insured, the covered property or claimant, the cause of loss, and the question's command word. If two answers are legally true, choose the one that answers the exact fact pattern.

If you miss the passing score, use the report as a map. Rebuild the two weakest content areas, then retest with mixed questions. Candidates often improve fastest by mastering policy architecture: declarations, insuring agreement, conditions, exclusions, definitions, and endorsements. Once you can locate where a rule lives inside the policy, unfamiliar questions become easier to reason through.